NHR 2.0 — How Portugal’s Selective Tax Haven Works

A policy analysis of how Portugal’s IFICI (former NHR) regime creates structural tax asymmetries between newly arrived residents and long-term local professionals doing the same work.

NHR / IFICIPolicy AnalysisTax Regime

▶️ Video explainer

Short visual breakdown of the key ideas, with narration and graphics.

🎧 Podcast

In-depth discussion expanding on the themes explored in this article.

What This Publication Is About

A simplified visual summary of the IFICI / NHR framework and the tax asymmetries explored in this publication.

This publication simplifies and interprets the IFICI regime based on public information. It aims to explain, in a clear and accessible way, how the IFICI tax regime — widely referred to as NHR 2.0 — works in Portugal and which mechanisms are used by new residents to drastically reduce their tax burden.

Through practical examples and direct comparisons, it shows how different structures — a single-shareholder company, a foreign holding company, an Employer of Record, or simply already having international clients — may allow a professional to pay only 20% in Portugal and, in some cases, even 0% on foreign-source income, when the necessary legal conditions, treaty rules, and interpretations are met.

The central purpose of this publication is to make visible, even to readers without technical tax knowledge, the scale of the inequality created by these arrangements when compared with standard tax residents in Portugal, who may pay up to 48% IRS on the same work.

The EURES portal (European Employment Services) identifies the visual arts and audiovisual production sector — including film directors and producers, photographers, and audiovisual technicians — as an area with insufficient job offers and greater difficulty for candidates seeking work in Portugal.

There is a clear irony here: the former NHR 1.0 and the current IFICI regime are promoted as tools to attract “talent”, yet by creating severe tax asymmetry and fiscally distorted competition, they can penalise the local professionals who already provide exactly the same services in Portugal, and may even push them out of the market.

If the policy objective is truly to benefit the sectors into which this talent is being drawn, why do official communications focus almost exclusively on research, science, and technology, while saying little or nothing about fields such as the arts and audiovisual production, which are also covered?

Meanwhile, indicative fee tables for audiovisual technicians — used for years as a market reference — were targeted in 2023 by the Portuguese Competition Authority, and the association that published them was fined and forced to remove them for allegedly contributing to price fixing. Yet the IFICI regime, written into the law itself, continues to permit a structural difference in taxation between new residents and professionals who have always worked in Portugal, creating fiscally distorted competition inside the same market.

This is not an isolated concern. Critics have also pointed to the regime's wider effects on housing, cost of living, and market pressure, particularly when preferential tax treatment for new residents increases purchasing power in a country where local wages remain much lower.

Important note: This publication focuses on IRS asymmetry, especially the contrast between 0%–20% for some newly arrived residents and up to 48% for long-term residents performing the same work. It does not replace professional tax or legal advice.

This is also not “zero tax” in an absolute sense. The exemption discussed here applies only to IRS. The new resident may still pay Social Security contributions on earned income and, where relevant, municipal property taxes such as IMT and IMI. In addition, structures such as holdings and EOR arrangements carry incorporation, maintenance, and compliance costs, and international tax positioning always requires specialised legal and tax advice.

Practical Example: A Director of Photography from Another Country Wants to Live in Portugal

Ben arrives in Lisbon to begin a new chapter — with sun, opportunity, and a very particular tax regime.

Character: Ben, a Director of Photography from another country.

Objective: He wants to move to Lisbon and pay the minimum possible tax using the IFICI regime.

Problem: He does not yet have foreign clients.

Solution: Consulting firms offer several legal “paths” to help him fit the regime.

Path 1 — A Sole-Shareholder Company in Portugal

Ben creates a Portuguese single-shareholder limited company.

He appoints himself Manager/Director, a role appearing on the list of eligible professions.

The consulting firm ensures that the company invoices more than 50% abroad; in practice, this may only require arranging some international contracts.

Result:

Work for Portuguese clients becomes Portuguese-source income and may benefit from the special 20% rate.

Work for foreign clients is often commercially presented as potentially being foreign-source income taxed at 0% IRS.

Note: Ben can come to Portugal with no clients and, once in Lisbon, begin by finding a few small assignments for foreign clients on his own. That can also count towards the condition that more than 50% of invoicing comes from abroad.

The IFICI guide issued by the Portuguese Order of Accountants states that, in order to apply the exemption method to category B income, a fixed installation or permanent establishment abroad is generally required.

If the work is carried out from Portugal, even for foreign clients, the income will generally tend to be treated as Portuguese-source and therefore not automatically exempt.

By creating a Portuguese single-shareholder company, Ben stops acting merely as a freelancer and starts offering services across the whole audiovisual field, functioning in practice like a production company capable of competing directly with local companies.

Direct Competition with Local Production Companies

Once he creates a sole-shareholder company, Ben ceases to operate merely as a freelancer and starts selling services like a genuine film and video production company. When he gets larger projects, he subcontracts local technicians — sound recordists, assistants, operators — and those costs become production costs borne by the company.

On paper, the tax framework makes it possible that:

Foreign clients: the income can be presented as foreign-source income and, in certain arrangements, come close to 0% IRS in Portugal, depending on where the service is effectively provided, on double taxation treaties, and on the Tax Authority's acceptance.

Portuguese clients: the qualified work Ben provides may, in principle, be taxed at the special 20% rate under IFICI instead of the progressive rates that, for local production companies, can reach around 48%.

Impact: this tax margin allows Ben to offer substantially lower final prices, even while covering all production costs.

Result: a difference in tax burden is created that, in some scenarios, can amount to several dozens of percentage points and which, in practice, functions as a form of fiscal dumping in a market already weakened by the shortage of employment in Portugal's audiovisual sector.

Path 2 — A Foreign Holding Company (for example, Malta)

The consulting firm creates a holding company in Malta.

That holding company opens a Portuguese subsidiary.

Ben employs himself in the Portuguese subsidiary and is taxed at 20% on salary.

Profits or dividends from the foreign holding may be paid to Ben with exemption in Portugal, provided treaty rules and economic substance rules are satisfied.

Result:

He satisfies the law formally by having a company, a qualified role, and residence.

But a large share of his income is turned into dividends that are not taxed in Portugal.

Creating and maintaining a holding structure in a country such as Malta may, in general, cost only a few thousand euros per year — registration, virtual office, accounting, company secretarial work, and similar overhead. Those amounts are within reach of many IFICI professionals who invoice tens of thousands of euros annually. It is therefore not merely an “exotic scheme for the elite”, but a standardised product that can become economically advantageous from income levels around €30,000 to €40,000, depending on the specific case.

Path 3 — Employer of Record (EOR)

Ben hires a consultant or EOR that creates an entity to “employ” him formally.

That entity invoices services abroad, even if the structure has been assembled specifically for that purpose.

Ben receives salary or fees framed under IFICI and therefore taxed at 20% IRS.

If he sells his business or has passive income, the consultant may “repackage” those flows into investment products, bringing the effective rate down to 2%–7% in some cases, depending on structure and tax acceptance by the authorities.

Result:

He meets the formal requirements.

But in practice he is using the consultant's structure in order to gain access to an exemption on foreign income.

Path 4 — Already Having Foreign Clients

Example: Ben already works regularly for production companies in his home country and decides to move to Lisbon.

Tax residence: Ben becomes resident in Portugal and applies for IFICI status.

Qualified activity: As a producer, director, or cinematographer, his profession can fit the IFICI regime as a qualified activity under Ministerial Order no. 352/2024.

Existing foreign clients: He continues to film in Portugal for production companies from his country of origin, invoicing them directly.

Tax declaration:

Although the clients are outside Portugal, Ben performs the work from Portugal. According to the IFICI guide from the Portuguese Order of Accountants, such income is generally Portuguese-source income and is therefore taxed in Portugal, not automatically taxed at 0% IRS.

The country of origin taxes only if, under the relevant double taxation treaty, it is allowed to do so — for example, if there is a permanent establishment in that country.

Result:

Work for Portuguese clients is taxed at 20% IRS.

Work for foreign clients may, in some forms of tax planning, come close to an effective burden of 0% IRS.

All of this can happen without a holding company or an EOR, simply by making use of clients he already had before moving.

In many of these commercial sales narratives, the idea offered to Ben is obvious: settle in Portugal, build foreign relationships and clients, provide them with services from here, and seek to frame that income as foreign-source income that may be exempt from IRS.

Path 5 — Minimum Passive Income

Example: Ben has regular foreign passive income — interest, dividends, royalties, or rents — adding up to at least €870 per month, the equivalent of the Portuguese minimum wage used here as an illustrative benchmark.

Tax residence: Ben becomes resident in Portugal and applies for IFICI status.

Qualified activity: A producer, director, or cinematographer may fit the IFICI regime as a qualified activity under Ministerial Order no. 352/2024. In addition, if Ben receives passive income from foreign sources — such as interest, dividends, royalties, or property rents — such income may, in certain cases, benefit from exemption in Portugal, although each type of income has its own rules and may also be subject to withholding tax in the country of origin. The €870 monthly figure is used here only as an illustrative benchmark for means of subsistence, not as a formal legal requirement.

Continuing to work: Ben continues to work in Portugal as a director or cinematographer. The services he provides, even to foreign clients, are generally taxed in Portugal, though he may benefit from the 20% IFICI rate if the regime applies.

Tax declaration:

After entering the regime through his passive income profile, Ben continues to work from Portugal. Even with foreign clients, that labour income is generally considered obtained in Portugal and taxed here, though it may benefit from the 20% rate.

More aggressive tax planning may attempt to build foreign structures in order to reclassify part of that work as foreign-source income and obtain exemption.

Result:

Work for Portuguese clients, and foreign work physically carried out from Portugal, is taxed at 20% IRS.

Foreign passive income may, in some cases, be exempt from IRS in Portugal.

This can happen without any holding company or EOR arrangement, simply through passive income Ben already had outside Portugal.

Comparative Table

Path

What Ben does

How it formally fits the law

What he pays

How it works in practice

Sole-shareholder company in Portugal

Creates his own company

Eligible role + more than 50% foreign invoicing

20% in Portugal; abroad may, in some cases, come close to 0%

Declares work for foreign clients as “foreign income”

Holding company in Malta

Creates a parent company abroad plus a Portuguese subsidiary

Employment in a qualified role

20% on salary; dividends may, in some cases, be exempt

Profits are distributed as exempt dividends

Employer of Record (EOR)

A consultant creates an entity that employs him

Exporting company + qualified role

20% on salary; investment-packaged income may, in some cases, be taxed at 2%–7%

Passive income is repackaged into investment products

Already having foreign clients

Continues invoicing clients from his home country

Qualified profession + residence

20% in Portugal; abroad may, in some cases, come close to 0%

Frames international invoicing as “foreign income”

Minimum passive income

Proves regular foreign passive income of at least €870/month

Residence + qualified profession

20% in Portugal and, in some cases, close to 0% abroad, including eligible foreign passive income

Uses passive income as a base of subsistence combined with IFICI

Conclusion.

Anyone who already has foreign clients only needs to fit the IFICI framework; the tax benefit can apply immediately.

Anyone who does not have such clients turns to consultants to build structures — sole-shareholder companies, holdings, or EOR arrangements — that simulate or generate international invoicing.

Anyone with foreign passive income may, in some cases, benefit from IRS exemption under IFICI, provided they are already framed through a qualified activity and tax residence.

In many cases, the desired effect is the same: 20% in Portugal, 0% abroad, provided all legal requirements and treaty rules are met.

IFICI is not fraud. But it is an invitation to inequality — flavoured with pastel de nata and 0% IRS.

Ben's Long Vacation

Living in Portugal while earning passive income from abroad — potentially with little or no IRS.

Living in Portugal on Foreign Passive Income

Ben receives passive income that could consist of rent from a house he lets in his home country, for an amount equal to or greater than one Portuguese minimum wage (€870 in 2025). Ben lives in Portugal and falls within the NHR 2.0 / IFICI regime.

Ben does not work and still has access to the social safety net and to public services financed by the taxes — IRS, VAT, and others — paid by the standard tax resident, while his own contribution in IRS may be 0%.

The regime was designed to attract qualified residents or people with financial means, not to verify whether they are actually active.

Reminder: consult a tax specialist; this text does not replace professional advice.

Search Results and Distorted Competition

Lower taxes allow Ben to offer lower prices — undercutting local competition.

An analysis of search results for specific terms related to the professions and services Ben provides illustrates the fiscally distorted competition created by NHR 1.0 and NHR 2.0. Those results are dominated by foreign professionals and international agencies acting as intermediaries, which further increases competition in the market.

Professionals like Ben, framed as “high added value” workers, may in certain specific structures reach an effective tax burden close to 0% — and in some cases actually 0% — on the income they invoice to clients based abroad. That gap of up to 48 percentage points gives them the margin to offer services in the low-to-mid-budget segment and thereby crush local competition.

The market becomes unsustainable for the long-term resident because the law ends up creating unequal tax competition within the country itself.

A Contradiction That Is Hard to Ignore

If the work is physically done in Portugal, why is the tax logic not the same for everyone?

If the serious criterion were the place where the work is actually performed, the Portuguese Tax Authority would have to apply the same logic to everyone: to the Portuguese director who has always lived in Lisbon and to Ben, the “new digital nomad”, sitting at a café table editing videos for a client in New York. In both cases, the work is carried out in Portugal.

And yet the IFICI regime opens an exception precisely for certain Bens, allowing a large part of that income to be treated as “foreign-source” and therefore potentially exempt from IRS, while long-term residents remain under normal taxation. Either the income is Portuguese for everyone, or it is foreign for everyone. Everything else is discrimination built into the law itself.

The use of foreign intermediary companies only makes the whole arrangement more artificial. In practice, it can work like this: the client is Portuguese, the work is done in Portugal, but the invoice comes from a foreign company for which Ben “works” — whether that company is a producer or a holding in a place such as Malta. That foreign company invoices Ben's client and then pays Ben. In the end, the entire income appears to come from abroad even though the work never left Lisbon.

As for content-based distinctions, there is no clear and objective legal criterion capable of saying: “up to this point it is documentary; beyond that it becomes advertising or corporate video.” In substance, it is all audiovisual production within the same professional family.

International Work and the "Loophole"

For many freelancers and local production companies providing the same services as Ben, international work is one of the main sources of income and growth. When the IFICI regime gives a far greater tax advantage only to newly arrived qualified residents, it creates unequal competition exactly in the space where domestic talent has been trying to grow.

Moreover, competition for the same clients does not stop at the international market: Ben can use this tax advantage to offer lower prices to Portuguese clients too, gaining an advantage in both markets.

In this example, by paying no tax in the client's country — being treated there as a non-resident under the relevant treaty, perhaps by means of forms such as the W-8BEN — and by being exempt in Portugal under IFICI/NHR, Ben can reach double non-taxation on his income.

The loophole sold commercially is the following: some consultants suggest that Portugal may exempt this income even when the client's country does not in fact tax it. Yet the IFICI Guide of the Portuguese Order of Accountants states that, as a rule, exemption for category B requires a fixed installation or permanent establishment abroad.

Put differently, the interpretation is that there may be IRS exemption provided that the income could have been taxed in the country of origin, even if it was not actually taxed there. Or, failing a double taxation treaty, provided that the income is not considered obtained in Portuguese territory. Proof that tax was effectively paid abroad is not required.

The loophole results from three legal pieces fitting together:

the double taxation treaty between Portugal and the country of Ben's client;

the absence of a permanent establishment for Ben in the client's country;

the IFICI / NHR status and the exemption method in Portugal for income considered “foreign-source”.

Portugal has signed treaties of this kind with 79 countries, so this is not an isolated possibility but an opening available across multiple jurisdictions.

The key point is that, for IFICI / NHR 2.0 purposes, the benefit on so-called foreign-source income does not result from a coherent application of the domestic rule based on where the work is physically performed. It results instead from the interpretive reading of the relevant double taxation treaty. In practice, that choice of criterion is what makes it possible to treat as “foreign” income generated by work physically done in Portugal.

One might say: “Go abroad without leaving home.”

And Inside Portugal?

The injustice does not disappear on the domestic side.

Imagine a purely domestic law saying: “Professionals who have worked in Lisbon during the past five years pay IRS at normal rates; professionals coming from Porto always pay a flat 20%.” The difference would be “only” eight or ten percentage points. Would anyone consider that acceptable, or would it immediately be seen as a blatant violation of equality?

Imagine a similar example for passive income. It would be as if the law said that a professional from Porto, after moving to Lisbon, would stop paying IRS on the rent from their house in Porto simply because they are now a “new resident” in the capital, while a person who has always lived in Lisbon would continue paying tax on identical rental income. Anyone would recognise that as an inequality that is hard to justify.

Why do we accept discrimination more easily when the criterion becomes “new resident” versus “long-term resident”?

In competitive markets, a difference of 5% can be enough to move competition. Injustice does not stop being injustice just because the gap is “only” 10% or reaches 48%.

This is not merely tax inequality capable of generating unequal competition. It is a regime that tends to create two categories of citizens for the same work.

Pause and Return

The IFICI regime can effectively be paused and resumed during its ten-year lifespan.

The IFICI regime can be “turned on and off” over its ten-year duration: just as someone can catch a bus and come back later, a new resident may leave Portugal for a few years and, upon becoming a tax resident again and resuming a qualified activity, recover the benefit for the years still remaining.

By contrast, a Portuguese professional or long-term resident who has always worked in Portugal has no access to this mechanism. In theory, in order to benefit from the same regime, that person would need to interrupt Portuguese tax residence for five consecutive years and only then return as a “new resident”. In practical terms, the system tells them: if you want the same tax conditions as Ben, leave for five years and then come back.

Regardless of whether work opportunities actually exist in Portugal, the regime is widely promoted to foreigners by market players — lawyers, consultants, real-estate actors — who simultaneously inform and prospect clients, directly affecting professionals in sectors where opportunities are already scarce.

Double Inequality: Tax + Time

The regime does not merely create inequality between new residents and standard tax residents. It also creates inequality between new residents today, new residents tomorrow, residents who left and return, and residents who never left.

A Portuguese citizen who has always lived here → does not have access.

A Portuguese citizen who leaves for five years → does have access.

A foreigner who arrives now → has access.

A foreigner who arrives three years from now → may face different rules.

This creates something very rare in tax policy: an inequality that depends on the calendar, not on the general law. It is literally a temporal lottery.

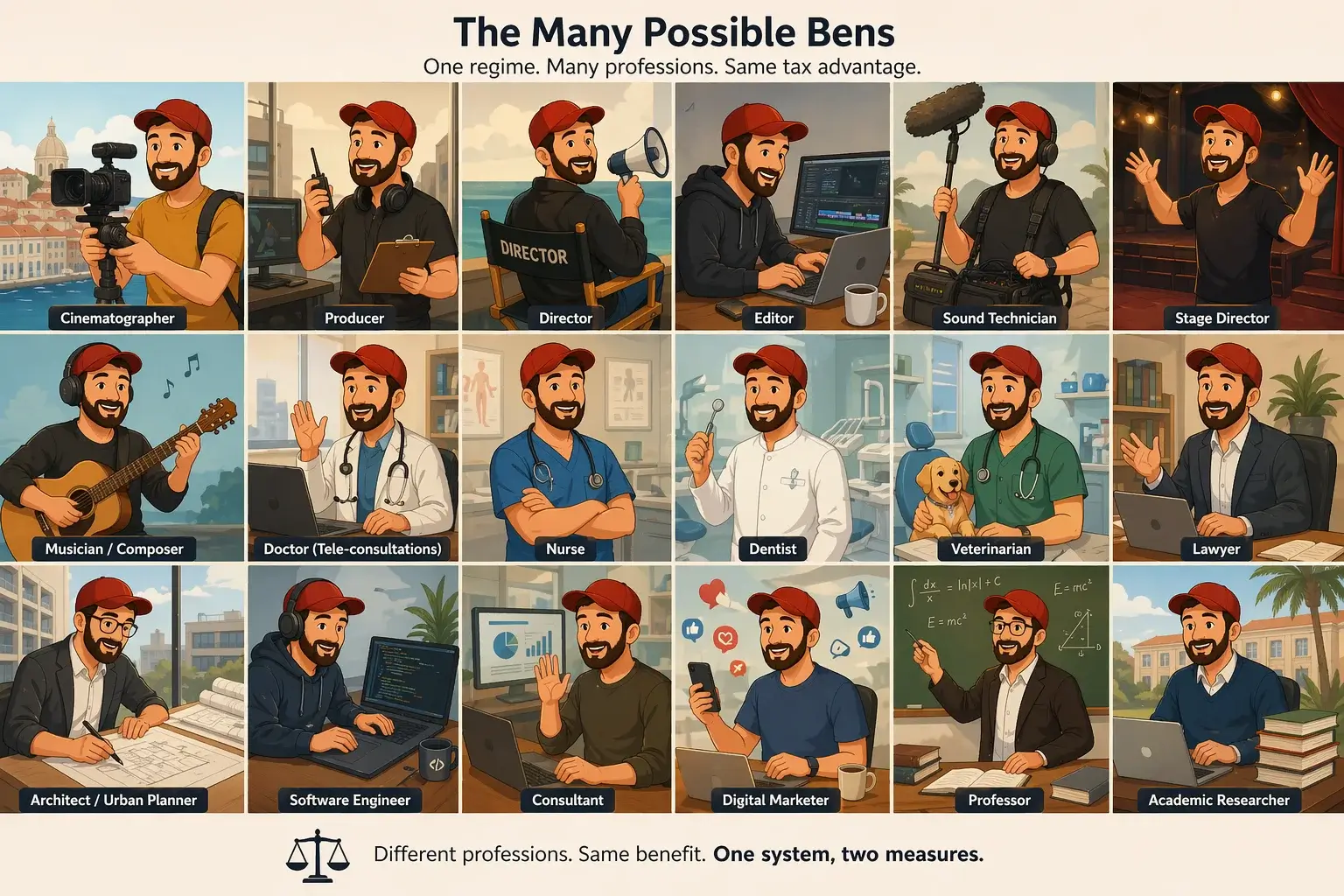

The Many Possible Bens

One regime, many professions — the same tax advantage applied across sectors.

Ben is fictional, but he is not unreal. Just as there can be Ben the cinematographer, there can also be Ben the producer, director, editor, sound technician, stage director, composer, or musician. There can be Ben the doctor providing tele-consultations abroad; Ben the nurse or dentist charging competitively; Ben the veterinarian opening a clinic in Lisbon; Ben the lawyer advising international companies; Ben the architect or urban planner designing projects for foreign clients; Ben the software engineer working remotely for multinationals; Ben the professor teaching in higher education while participating in international academic programmes.

The list of possible Bens is extensive. These many Bens are possible because the regime leaves room for new residents, across multiple fields, to enjoy far more favourable tax conditions than those available to professionals who have always lived and worked in Portugal. The result is a structural inequality affecting professionals in many sectors, weakening those who were already here and competing under ordinary conditions.

In practice, this may also create an economic incentive for companies to favour the hiring of these new residents over local professionals carrying a higher tax burden, and for rates and wages to be pushed downward, since someone who pays much less tax can accept lower prices without losing net income. This dynamic may be especially attractive to consultants and intermediaries involved in promoting these regimes, as they can benefit economically from each new client entering the framework.

Whatever capital these regimes may bring to the country, a just law should be effective without creating inequalities or discriminating against some citizens. The gains can be assessed in percentages and numbers; justice cannot. Justice should not take such gains into account but should instead look at how the law treats people who are within the same system.

At bottom, each Ben is just an example of how the law creates two weights and two measures within the same country.

Intersectoral Asymmetry: Some Sectors Are Crushed, Others Barely Feel It

The regime does not affect all sectors equally.

It is devastating in sectors where:

there is a great deal of international mobility,

there is remote work,

services are digital,

average salaries are relatively low,

there are many freelancers and independent workers,

and there is global competition.

Examples include audiovisual work, design, software engineering, consulting, digital marketing, architecture, music, and internationalised higher education.

By contrast, the regime is almost irrelevant in sectors such as construction, hospitality and restaurants, agriculture, and local retail.

In other words, the regime creates winners and losers within the economy, and the losers are precisely the creative and technical sectors that were already fragile.

The Hidden Impact of IFICI on Employees: The Mathematics of Exclusion

The balance is tilted before the work even begins: under IFICI, Ben can become cheaper to hire than Zé for the same net outcome.

Up to this point, this publication has focused mainly on freelancers and independent workers. But the IFICI / NHR 2.0 regime may have an even more structural impact on dependent employment — an impact that does not rely on tax planning, consultants, or international structures. It depends only on one simple difference:

The standard tax resident is taxed according to progressive IRS brackets.

The new IFICI resident may receive a flat 20% rate on the same type of labour income (category A), provided the work falls within an eligible activity.

For the worker, what matters is net salary. For the employer, what matters is the total cost: gross salary plus the employer's Social Security contributions.

If two workers — Zé, the standard tax resident, and Ben, the new IFICI resident — both want the same net monthly income, the company will generally have to spend substantially more on Zé.

The Mathematics of Exclusion: Gross vs Net

Let us assume an illustrative example: two qualified professionals who want to take home around €2,500 net per month.

Important note: the numbers below are simplified estimates used to illustrate the logic. They do not replace an official calculation that takes into account all deductions, tax brackets, Social Security contributions, and individual circumstances.

Component

Zé (standard tax resident)

Ben (new IFICI resident)

Desired net salary

€2,500

€2,500

IRS regime

Progressive brackets (e.g. ~35%)

Flat 20% rate

Required gross salary

~€4,300

~€3,400

Employer Social Security contributions

~€950

~€750

Total cost to employer

~€5,250

~€4,150

Difference in cost to employer

—

-€1,100 / month

Total cost equals gross salary plus the employer's Social Security contributions.

Practical result: to guarantee the same standard of living in net terms, the company spends hundreds of euros less per month by hiring a Ben instead of a Zé. Across teams of 10, 20, or 50 people, the difference becomes tens or hundreds of thousands of euros per year.

This is not opinion. It is arithmetic applied to an asymmetrical tax regime.

The Central Contradiction: Revitalise or Replace?

IFICI is a tax regime for individuals — whether self-employed or employed. It is not an incentive for audiovisual production itself: it does not bring more films, more series, or more campaigns, and it does not increase demand. For that purpose there is already the cash rebate, which lowers the cost of filming in Portugal for foreign producers and platforms. IFICI acts only on the personal income tax side. In a sector that EURES itself identifies as having scarce job offers, bringing in more Bens with aggressive tax advantages does not create new work; it simply increases competition for the little work that already exists.

The argument that the regime “improves the sector” is a fallacy if it ignores the fact that the vitality of a sector depends on the survival of its foundational professionals — the people who have kept the infrastructure alive for decades. If the regime serves only to replace resident technicians with technicians discounted by tax, then it is not dynamisation but erosion of the national professional fabric.

It is like giving fuel discounts only to foreign truck drivers operating in Portugal and expecting that to help Portuguese truck drivers. The outcome is not dynamisation; it is downward pressure on rates, wages, and conditions for those who were already here.

If the objective were truly to reinforce the audiovisual sector as a strategic field, the fairer and more effective solution would be tax neutrality: a similar framework for all qualified professionals in the field — both standard tax residents and new residents — lowering the cost of services across the board in order to attract investment and production, while avoiding the creation of tax castes inside the same professional family.

Why Does This Push Standard Tax Residents Out of the Labour Market?

1) Hiring Preference

If a company needs to hire ten engineers, designers, audiovisual technicians, or analysts, it has two options:

hire Zés → much higher total cost,

hire Ben → much lower total cost for the same net salary.

In a context of tight margins and global competition, the economic incentive naturally pushes the employer towards Ben.

2) Silent Labour Replacement

A company does not need to announce that it is “replacing Portuguese workers with foreigners”. It only needs to:

not renew the contracts of standard tax residents,

not promote them,

not update gross salaries in line with the cost of living,

and fill new vacancies with people who qualify for preferential regimes.

The result is gradual replacement: the standard tax resident becomes “expensive” in Excel even when they are an excellent professional. The company does not replace them out of prejudice; it replaces them because the spreadsheet tells it to do so.

3) Structural Wage Dumping

Ben knows that:

he pays 20% IRS on salary,

and that in some more sophisticated international planning scenarios — involving capital income, structures outside Portugal, and double taxation treaties — the effective burden on part of his income can come close to 0%, or in very specific situations actually reach 0%.

None of this automatically implies illegality. It means only that the tax framework creates asymmetries that distort the market.

That gives Ben room to accept a gross salary that Zé will struggle to match, because for Ben, 20% IRS and possibly lightly taxed additional income still produce a comfortable net result, while for Zé, the same gross amount, filtered through progressive brackets and lacking such advantages, results in a much lower net amount.

The wage floor of the sector falls in order to accommodate Bens. The person who is crushed between the cost of living and progressive taxation is Zé.

Conclusion: An Indirect State Subsidy for Hiring “New Residents”

IFICI / NHR 2.0 is not merely a tax advantage for Ben as an individual. In practice it also functions as a financial advantage for the company that hires him:

the State gives up revenue by applying 20% instead of the normal, much higher rates,

the company can hire qualified talent at a significantly lower total cost,

the standard tax resident, lacking access to the regime, becomes “too expensive on paper” — not because they work worse, but because they pay Portuguese taxes under less favourable conditions.

The aggregate effect is a structural marginalisation of the standard tax resident employee within the labour market.

Those who have always lived here and always paid into the system are placed at a disadvantage relative to those who arrive under a preferential tax framework, often with the support of consultants and international structures that maximise the difference still further.

IFICI does not create only tax inequality — it creates wage inequality. And that inequality is not between companies. It is between people.

The regime increases geographic inequality.

It pushes local residents out of city centres.

It accelerates gentrification.

It creates tax islands within the country.

The Importation of Qualified Labour

In parallel with IFICI, Portugal changed its immigration law in order to privilege the entry of “highly qualified” workers, creating specific channels within AIMA and even a “talent department”. In several public statements, the IFICI regime itself is referred to as a benchmark for defining such activities, bringing migration policy closer to the same fiscal logic used to attract newly arrived qualified residents.

In practice, this can open the way for companies in areas such as IT, technology, or specialised services to transfer entire teams to Portugal, combining preferential migration channels with more favourable tax treatment for those new residents. It is a kind of reverse offshoring: instead of sending work to lower-wage countries, workers from those countries are brought into Portugal itself, where they then compete directly with local professionals who remain subject to ordinary taxation.

Generational Asymmetry: Young Portuguese vs Young Foreign Residents

A young Portuguese person

starts a career on low wages,

pays progressive IRS,

pays rent inflated by the arrival of Bens,

has no access to the regime,

and cannot compete with Ben's higher net salary.

A young foreign resident

arrives with a high net salary,

pays 20%,

has greater purchasing power,

enters directly into qualified positions,

and pushes the market upwards — but only for some people.

This creates a generational inequality that is not merely economic; it is symbolic as well.

Institutional Asymmetry: The State Finances Inequality

The State:

gives up tax revenue from Bens,

but continues to demand progressive IRS from Zés,

uses that revenue to finance services that Bens also use,

and still benefits from the consumption generated by Bens.

In other words:

the State creates inequality,

the State finances inequality,

and the State legitimises inequality.

Conclusions

IFICI creates two categories of workers inside the same country. For the same work, a standard tax resident may pay up to 48% IRS while a new resident pays 20% — or may, in some cases, come close to 0% if they manage to frame that income as “foreign-source”.

The inequality is not only fiscal — it is economic, labour-based, and structural. Whoever pays less tax can charge less, accept less, and compete unfairly with those who have always lived and worked in Portugal.

The regime allows Portuguese income to be transformed into “foreign income”. Through holdings, EOR structures, intermediary companies, or simple international framing, work carried out in Lisbon can be made to appear as income coming from abroad.

The State gives up Ben's tax revenue and demands more from Zé. The difference does not disappear; it is paid for by the standard tax resident who remains under progressive taxation.

The regime creates an economic incentive to replace Zés with Bens. To deliver the same net salary, a company spends hundreds of euros less per month if it hires a Ben. Across large teams, the savings become enormous.

The inequality is also temporal: it depends on the calendar, not on justice. A Portuguese citizen who has always lived here cannot access the regime; a Portuguese citizen who leaves for five years and comes back can. It is a tax lottery.

Some sectors are crushed while others barely feel the impact. Audiovisual work, design, consulting, software, music, architecture, and international education are among the most affected. Construction, restaurants, and local retail hardly benefit or compete under the same conditions.

Ben's arrival raises the cost of living without increasing opportunities for Zé. Companies that move to Portugal often bring their own teams rather than hiring locally. But housing and service prices rise for everyone.

The regime creates wage dumping and distorts the internal market. Whoever pays 20% or 0% can accept amounts that a standard tax resident cannot match. The wage floor falls while the cost of living rises.

In the end, the regime does not attract talent to Portugal — it attracts inequality into Portugal. The country gains consumption and statistics; Zé gets inflation, unequal competition, and a loss of competitiveness in his own market.

While many Bens settle comfortably, Zé is the one who ends up leaving.