Portugal NHR 2.0 (IFICI): How the Tax Regime Really Works

Portugal’s IFICI tax incentive regime explained in clear language. What consultants, tax lawyers and technical guides present as an opportunity for new residents — and the mechanisms, limits and structural asymmetries affecting local professionals that the public narrative tends to omit.

NHR 2.0 / IFICIPolicy AnalysisTax Regime

▶️ Video explainer

A simplified visual walkthrough of how Portugal’s TISRI (NHR 2.0 / IFICI) regime works in practice — following the path of a typical high-skilled professional and contrasting it with the reality faced by long-term local residents. By breaking down the mechanics step by step, the video highlights how identical work can be taxed in fundamentally different ways, and how those differences translate into real economic incentives that reshape hiring decisions, wages, and competition.

🎧 Podcast

An in-depth discussion of how IFICI works, the gap between new and long-term residents, and its practical effects on work, wages and housing.

What This Publication Is About

A simplified visual summary of the TISRI (NHR 2.0 / IFICI) framework and the tax asymmetries explored in this publication.

This publication simplifies and interprets the IFICI regime based on public information. Its aim is to explain, in a clear and accessible way, how Portugal's IFICI tax regime — commonly referred to as NHR 2.0 — works and which mechanisms are used by new residents to significantly reduce their tax burden.

Through practical examples and direct comparisons, it shows how different structures — a single-shareholder company, a foreign holding company, an Employer of Record, or simply already having international clients — may allow a professional to pay 20% in Portugal and, in some cases, achieve a very low or even 0% effective tax burden on foreign-source income, when the applicable legal conditions and treaty rules are met.

In the case of certain categories of foreign-source passive income, this outcome does not constitute an exception but rather a normal consequence of how the regime applies under the legal framework, being described in legal analyses as a broad exemption framework under specific conditions.

The contrast begins with the programme’s official name: Tax Incentive for Scientific Research and Innovation (IFICI). This breadth is not merely a critical interpretation. A Pérez-Llorca legal briefing on qualified job positions and economic activities recognised by AICEP/IAPMEI confirms that IFICI may cover general managers, executive managers, corporate officers, finance specialists, ICT professionals, as well as hospitality, restaurants and similar activities, holding companies and licensed fund management.

When “innovation” comes to include hotel management, restaurants, holding companies, consulting and fund management, the name of the regime no longer clearly describes its practical scope and also starts to function as a narrative of legitimation.

That name contains a measurable promise: more research, more innovation, more science in Portugal. This publication examines how the regime works in practice, who benefits from it, and what is known — and not known — about whether it is delivering what it promised.

ℹ️ Important limitation on tax risks

Some of the structures described — particularly those involving foreign companies — may be reviewed by the Portuguese Tax Authority. Concepts such as effective management, permanent establishment, CFC rules and anti-abuse provisions may affect the acceptance of these arrangements. This publication reflects how these strategies are presented in the market and in public materials, and does not imply that all configurations are risk-free or automatically compliant.

Some commercial explanations of the regime explicitly highlight the use of international structures, corporate entities, and pre-move tax planning as key elements in accessing Portugal’s TISRI (NHR 2.0 / IFICI) framework — made possible by its reliance on formal eligibility criteria rather than prior case-by-case approval. While often presented in terms of employment income, the most significant effects of the regime arise in relation to foreign passive income and capital gains.

The supporting evidence, official notices and institutional sources are available below for readers who want to verify the legal and documentary basis before moving to the practical example.

📊 How the regime is presented in practice (real-world examples)

How the regime is presented by the private sector

Beyond video explainers and publicly available materials, similar outcomes are also described in written publications produced by tax advisory firms.

A 2026 publication by a tax advisory firm, authored by a Head of Tax, states that under the NHR 2.0 / IFICI regime:

“This will give you: A complete exemption on virtually all foreign-source income.”

The same source also clarifies that access to the regime may involve working through a Portuguese company, including one owned by the individual:

“the new NHR 2.0 (IFICI) also requires that you work for a Portuguese company (even if that’s your own company)”

In an official Touchdown video, a Portuguese tax lawyer explains that a person carrying out a qualifying activity may create their own company in Portugal, become its manager or employee and provide services to existing clients through that structure.

When describing the resulting tax treatment, he states:

“Everything you move through Portugal, 20%. Everything abroad is zero, including capital gains, dividends, interest income, rental income.”

The presenter then characterises the regime as:

“Probably one of the most lucrative and attractive tax regimes in the developed world.”

A similar interpretation appears in another publication aimed at internationally mobile taxpayers, which presents the new regime as an opportunity to obtain reduced taxation in Portugal through qualifying activities and Portuguese corporate structures.

" The new scheme is somewhat more complex in terms of its structure, but it is generally more favorable than the old scheme , because, for example, profits on shares (so-called capital gains) are now also exempt."

This reading is reflected across international financial media. A World Finance article frames IFICI within the context of record global wealth migration. In other words: a regime officially designed to foster science and innovation appears, in the international market, positioned as a key catalyst for attracting high-net-worth individuals (HNWIs). The article stresses that access to the regime requires careful structuring, framing IFICI as a central element in a broader offering of tax planning and corporate structuring.

“Portugal leads Europe’s millionaire migration boom. Portugal is emerging as Europe’s leading magnet for high-net-worth individuals, thanks to its new tax regime for innovation and research, lifestyle appeal and strategic access to the EU.”

Projected net flows of high-net-worth individuals (HNWIs) for 2025. Portugal appears among the leading global destinations, with +1,400 millionaires and USD 8.1 billion in associated investable wealth. 📊 Source: Henley Private Wealth Migration Report 2025.

“For someone with existing offshore wealth structures (Channel Islands, Isle of Man, offshore investment managers), this is straightforward. For those without existing structures, it requires establishing them before relocation.”

The logic of pre-move structuring is laid out here with unusual clarity. In this reading, IFICI does not merely accommodate foreign-source wealth — it appears to favour those who already have international wealth structures or can create them before becoming tax resident in Portugal.

The commercialisation of structures tailored to the regime is also publicly visible among corporate service providers. In an article by 1st Step Solution, the incorporation of a Maltese company is presented as an optimised solution for Portugal residents under IFICI. The text describes Malta as a European jurisdiction with an effective corporate tax rate that may be close to 5% in certain scenarios, with no withholding tax on dividends distributed to non-residents. This architecture confirms that IFICI operates, in practice, not only as an individual tax residence regime, but also as a cross-border corporate structuring product.

The “Malta + IFICI” structure helps illustrate the mechanics behind the 35% rule. Portuguese law applies this rate to income arising from jurisdictions listed as having clearly more favourable tax regimes — the so-called “blacklist” of tax havens. In practice, if income destined for an IFICI / NHR 2.0 beneficiary first passes through a company in a European jurisdiction that is not on that list, such as Malta, the entity formally paying the dividend changes. That formal change may allow the income to reach Portugal within the IFICI exemption framework. In simple terms: capital may originate in a fiscally privileged jurisdiction, pass through a Maltese holding company, and be received by the beneficiary under a more favourable tax classification — potentially benefiting, in certain cases, from personal income tax exemption.

This grammar of optimisation is also discussed in international technical forums. In a Portugal Pathways webinar on IFICI, featuring specialists from BDO and CMS Law, the regime is examined through its two central dimensions: the 20% flat rate and the exemption for foreign-source investment income and capital gains. The panel highlights a scenario of technical double non-taxation: the possibility that a capital gain or dividend may not be taxed in the source country, due to the application of bilateral tax treaties, while also benefiting from exemption in the hands of the Portuguese tax resident.

The structural question is simple: if the stated purpose of tax treaties and special regimes is to avoid double taxation, why can certain combinations produce practical double non-taxation? And why, in certain arrangements, can an exemption depend on the possibility of taxation abroad without always requiring proof that tax was effectively paid outside Portugal?

These commercial descriptions do not emerge in a vacuum: the Portuguese Tax Authority’s own official documentation confirms the central elements that make these outcomes possible, including the special 20% rate, the general exemption for foreign-source income, and the inclusion of corporate structures, management roles, and certain financial, consultancy and holding activities.

While advisory materials often present simplified outcomes, technical publications describe the regime in more precise legal terms:

Legal publications describe the regime in the following terms:

“Exemption from personal income tax on foreign-source income, including employment income, investment income (such as interest and dividends), rental income and capital gains.” (with certain exclusions, such as pensions and income from blacklisted jurisdictions)

“The exemption is granted without the need to verify the taxing-right allocation rules provided for in double taxation treaties.”

These descriptions coexist with the application of a 20% flat rate on qualifying Portuguese-source income, highlighting a structural distinction between domestic and foreign taxation.

In this respect, the current IFICI framework may in some cases be more permissive than the original NHR regime, particularly regarding the direct exemption of certain foreign capital gains, as noted in multiple legal analyses.

Beyond legal and institutional descriptions, international advisory firms frequently frame the IFICI regime in terms of tax efficiency and cross-border structuring opportunities, particularly for globally mobile professionals, founders, and investors.

In these contexts, Portugal is often positioned as a strategic destination for optimizing international income flows and coordinating business activity across jurisdictions.

Legal analysis also suggests that the scope of the IFICI regime may be broader than its name implies, including qualified roles within corporate structures, such as members of governing bodies.

These descriptions reflect how the regime is simultaneously marketed in practice and framed in legal and technical documentation.

The complexity of the legal framework, combined with interpretative flexibility, creates space for structured tax planning, typically mediated by specialised advisors.

The key issue is therefore not the existence of the regime itself, but the extent to which its outcomes may vary depending on how it is structured in practice.

⚖️ What the law actually says (official IFICI framework)

The official IFICI framework (Article 58-A and Notice No. 4812/2025/2)

The IFICI regime, established under Article 58-A of the Portuguese Tax Benefits Statute, is operationalised through administrative regulations published in the Official Gazette and official notices issued by IAPMEI, which define the concrete eligibility criteria.

Notice No. 4812/2025/2, published in the Official Gazette and made available by IAPMEI, explicitly defines the qualified roles and economic activities considered relevant for access to the regime under subparagraph (d) of paragraph 1 of Article 58-A.

Official confirmation from the Portuguese Tax Authority.

The Portuguese Tax Authority’s information leaflet on IFICI confirms that the regime combines a special 20% tax rate on qualifying Category A and B income obtained in Portugal, for 10 years, with an exemption, as a general rule, on foreign-source income in Categories A, B, E, F and G — including employment or self-employment income, investment income, rental income and capital gains.

The same document also establishes an important fiscal boundary: foreign-source income paid or made available by entities domiciled in countries, territories or regions subject to clearly more favourable tax regimes does not benefit from the general exemption and is taxed at a 35% rate. This distinction makes the qualification of the paying entity and the jurisdiction of origin a central element in international tax planning associated with the regime.

The same document also confirms that the regime may cover members of corporate bodies, administrators, managing directors and general directors, as well as financial and insurance activities, consultancy, head-office activities, holding companies and entities linked to tax incentives for business research and development.

In simple terms: although the regime is publicly presented as an incentive for scientific research and innovation, the official list shows that its practical scope can extend far beyond researchers or scientists, covering managers, administrators, consultants, holding companies and corporate structures.

The link between IFICI and entities benefiting from tax incentives for business research and development shows that the regime may operate in articulation with tax benefits at the corporate level. This reinforces the need to analyse IFICI not merely as a special personal income tax rate for individuals, but as part of a broader architecture of tax incentives that can combine advantages in both the personal and corporate spheres.

This combination raises a central question: if the regime is officially presented as an incentive for scientific research and innovation, why can its practical application cover administrators, managing directors, members of corporate bodies, holding companies, consultancy, financial activities and corporate structures? It is not merely a reduced rate on qualified work, but an architecture that combines a broad exemption for foreign-source income, management roles, corporate structures and business incentives. As a result, its distributive and competitive effects may differ from — and potentially be more intense than — those observed under the previous NHR regime.

This architecture also creates a direct incentive for tax-category arbitrage. When certain employment or professional income is taxed at 20%, while dividends, interest, rents, capital gains or other foreign-source income may benefit from exemption in Portugal, the system encourages income flows to be reorganised into the most favourable tax categories. The issue is therefore not only the applicable rate, but the ability to transform the legal and fiscal nature of income through corporate, financial or contractual structures.

What the official document establishes:

Eligible economic activities: Annex B explicitly includes financial and insurance activities, classes 6420 (holding companies) and 6630 (fund management), alongside sectors such as construction, hospitality, commerce, consultancy, and information technology.

Eligible roles: Annex A includes executive functions such as managing directors, senior managers, and company administrators, explicitly recognising administrators, managers, and general directors as qualifying positions.

Covered professions: The list explicitly includes audiovisual roles such as film, television, and radio directors and producers.

Minimum qualification: Within the scope of this notice, the requirement corresponds to Level 5 of the European Qualifications Framework. Other IFICI pathways, including highly qualified professions under Ordinance No. 352/2024/1, may require higher qualifications.

The notice itself says that the list largely comes from the previous NHR regime, with some adjustments.

In other words, the regime’s administrative architecture relies heavily on declarative validation. The Portuguese Tax Authority’s leaflet clarifies that, for certain categories — such as highly qualified professions under subparagraph (c) — beneficiaries do not need to submit initial supporting documentation. Confirmation is requested electronically from the company where the activity is carried out. Access to the regime can thus begin with a declaration by the entity itself, subject to possible later verification.

This model creates a critical time gap between access to the tax benefit and effective verification. Corporate structures may benefit from a fiscal and competitive advantage from the outset on the basis of formal declarations, while the verification of economic substance, main activity and real eligibility may occur only years later. Even if a configuration is eventually challenged by the Portuguese Tax Authority, its market effects — on prices, margins, hiring and competition — may already have taken place and may be difficult to reverse.

Notice No. 9709/2025/2, of 10 April 2025, further clarified that eligible CAE codes — including 6420, relating to holding companies — are only recognised when they correspond to the company’s main activity, and not to a secondary activity.

The holding route is often presented as more stable and predictable than the startup route. The startup status in Portugal is valid for periods of three years, automatically renewed by Startup Portugal but subject to periodic checks; moreover, the company has a legal duty to report within 30 days if it ceases to meet the requirements. A well-structured holding, when its main activity falls within the eligible codes and meets the applicable requirements, can offer a much stronger legal basis to maintain the 10-year tax benefit, without depending on the same recurring evaluation logic associated with innovation or the startup status.

How the regime works in practice is defined in Ordinance No. 352/2024/1, published in the Official Gazette.

These documents define the administrative framework and practical application criteria of the regime.

📄 Independent studies and institutional sources

Legal framework, studies and institutional sources

The legal framework of the regime can be consulted in the Diário da República, which formally defines the taxation of Non-Habitual Residents, establishes the right to a special tax status for a period of 10 years, and explicitly recognises that certain categories of foreign-source income — including capital income and capital gains — may be excluded from taxation in Portugal.

The framework described in this publication is aligned with research by the Bank of Portugal (Teles & Alpizar, January 2026), which identifies the main effects of the Non-Habitual Residents (NHR) tax regime.

Note: The available empirical data refers to the original NHR regime (2009–2023). While IFICI is technically distinct, it shares comparable structural characteristics and, in some aspects — particularly regarding the exemption of foreign-source income — may be even more permissive, according to recent legal analysis.

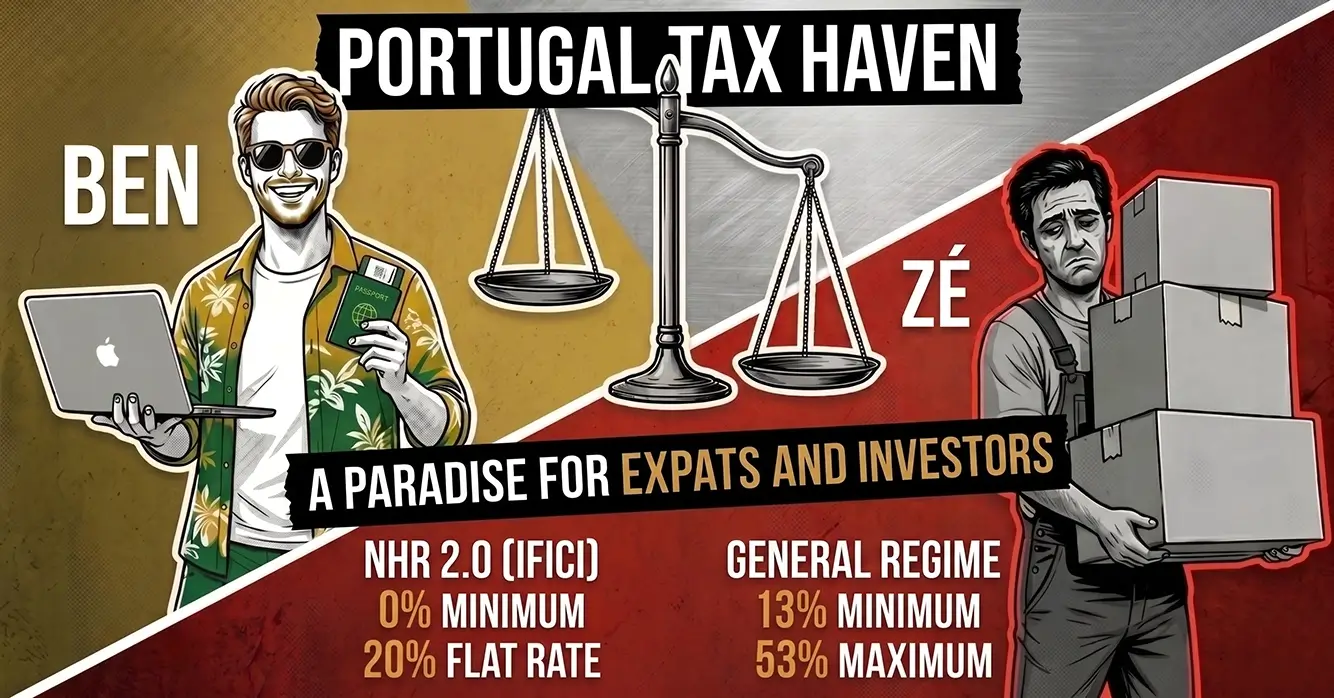

The study confirms the existence of a preferential tax regime with a flat 20% rate for certain types of income, in contrast with the progressive general regime which can reach levels close to 53%.

Data show that the main beneficiaries are at the top of the income distribution, with average levels significantly above the national mean, highlighting a concentrated impact on high-income individuals with international mobility. This composition also highlights a gap between the public narrative of attracting scientific or research talent and the observed profile of beneficiaries, where senior executive roles appear prominently.

The analysis also notes relevant distributive effects, especially in contexts of international tax competition, where gains tend to concentrate among highly skilled workers, potentially creating pressures on others.

🎙️ Bank of Portugal podcast on the former NHR regime

On 16 April 2026, Banco de Portugal published an episode of the BdP Podcast on the Non-Habitual Resident regime, based on the study “Residentes Não Habituais: impostos preferenciais para altos rendimentos em Portugal”, by Pedro Teles and Laura Alpizar.

Listen to the Banco de Portugal podcast episode referenced in this section:

The episode discusses the evolution of the regime, the exemption of foreign-source income, the 20% flat tax, the profile of the main beneficiaries, the fiscal cost and the distributive effects of international tax competition.

The study was also reported in the economic press, highlighting that the benefits were concentrated among the highest earners, particularly the wealthiest taxpayers.

Academic research has also analysed the regime from a sociological perspective, framing it within broader dynamics of international tax competition and highlighting its potential to generate internal inequalities between different groups of residents.

International legal analysis also describes the IFICI regime as maintaining a broad exemption for foreign-source income under certain conditions, alongside a 20% flat rate on qualified income.

Leading Iberian law firms have also confirmed that the IFICI framework combines a 20% flat rate on qualifying employment income with the possibility of exemption on most foreign-source income, subject to specific conditions and classification.

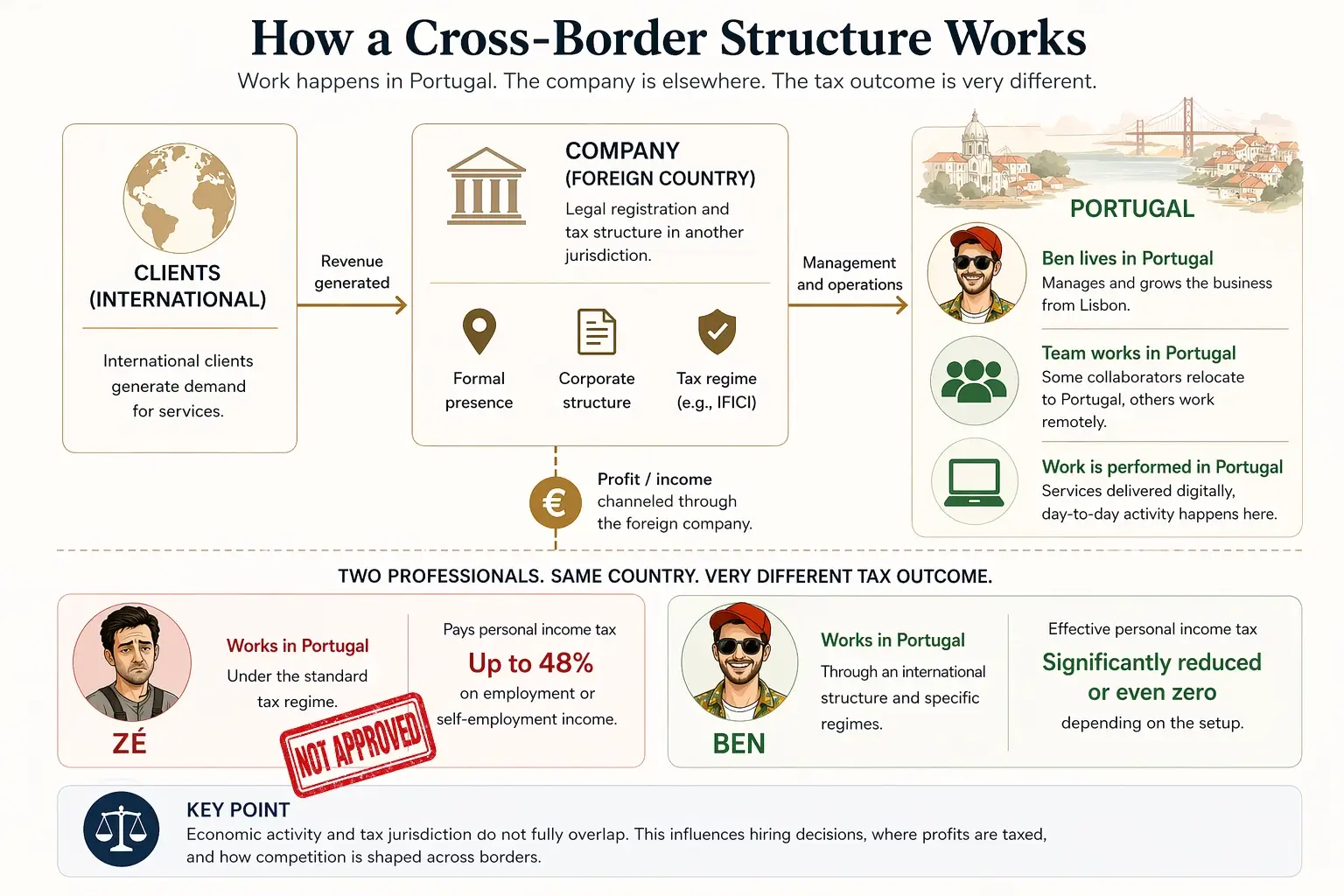

The central purpose of this publication is to make visible, even to readers without technical tax knowledge, the scale of the inequality created by these arrangements when compared with standard tax residents in Portugal, who may pay up to 48% Portuguese personal income tax (IRS) on the same work.

ℹ️ Clarification on the 48% tax rate

The 48% figure refers to Portugal’s top marginal IRS rate, not the effective tax rate applied to total income. Portugal uses a progressive tax system, meaning lower portions of income are taxed at lower rates. The comparison in this publication highlights the structural asymmetry between the general regime and situations where a flat 20% rate or exemption on certain foreign-source income may apply.

The EURES portal (European Employment Services) identifies the visual arts and audiovisual production sector — including film directors and producers, photographers, and audiovisual technicians — as an area with insufficient job offers and greater difficulty for candidates seeking work in Portugal.

There is a clear irony here: the former NHR 1.0 and the current TISRI (NHR 2.0 / IFICI) regime are promoted as tools to attract “talent”, yet by creating severe tax asymmetry and fiscally distorted competition, they can penalise the local professionals who already provide exactly the same services in Portugal, and may even push them out of the market.

If the policy objective is truly to benefit the sectors into which this talent is being drawn, why do official communications focus almost exclusively on research, science, and technology, while saying little or nothing about fields such as the arts and audiovisual production, which are also covered?

Meanwhile, indicative fee tables for audiovisual technicians — used for years as a market reference and contextualised in this sector manifesto — were investigated by the Portuguese Competition Authority in a process that culminated in a sanctioning decision in 2024. The association that published them was fined and required to remove them after the tables were considered a form of “price fixing”. Yet the TISRI (NHR 2.0 / IFICI) regime, written into the law itself, continues to permit a structural difference in taxation between new residents and professionals who have always worked in Portugal, creating fiscally distorted competition inside the same market.

This is not an isolated concern. A published opinion article (in Portuguese) has pointed to the regime’s wider effects on housing, cost of living, and market pressure, particularly when preferential tax treatment for new residents increases purchasing power in a country where local wages remain much lower.

This link between preferential taxation and the real estate market is also visible in the way the regime was circulated by actors within the sector itself. For example, a now-removed publication on the website of a Portuguese real estate agency specialising in the market for foreign buyers presented IFICI / NHR 2.0 as relevant information for foreigners considering residence in Portugal and making financial decisions in the country. The publication was dated 23 December 2024, the same day Ordinance No. 352/2024/1 was published, regulating the regime. Although the page reproduced information originally published by The Portugal News , its appearance on the agency’s own website shows how quickly the new tax benefit was treated as commercially relevant information for an audience of prospective international residents and property buyers. This does not, by itself, prove a direct impact on housing prices.

ℹ️ Important note on “0%” and the scope of this analysis

This publication starts from the personal income tax asymmetry, especially the contrast between 0%–20% for some new residents and up to 48% for tax residents under the general regime doing the same type of work. In later sections, the analysis also expands to company structures, social security contributions, business incentives and tax-framing mechanisms that may reinforce that advantage.

References to 0% scenarios are based on public information made available by tax advisers, business organisations and institutional materials — for example, publications by chambers of commerce. This content is analytical in nature and does not replace professional tax or legal advice.

In simple terms, IFICI is framed by Article 58-A of the Tax Benefits Statute, but the mechanism behind the exemptions on foreign income appears in Article 81 of the Portuguese Personal Income Tax Code. That is where the law provides that certain income obtained abroad may benefit from the exemption method in Portugal, while still being counted to calculate the rate applied to other income.

Even when certain foreign income benefits from a direct IRS exemption in Portugal, this does not mean that it disappears from a tax perspective. It may still have to be declared and, in some cases, may count when calculating the rate applied to other income. This is what is meant by progressivity or aggregation: the income may not pay IRS directly, but it may still be considered when calculating the IRS rate applied to the remaining income. Therefore, in this publication, “0%” should be understood as a reference to direct exemption on certain income — not as a complete absence of declaration, analysis or tax impact.

This is also not “zero tax” in an absolute sense. The exemption discussed here applies only to IRS. The new resident may still pay Social Security contributions on earned income and, where relevant, municipal property taxes such as IMT and IMI. In addition, structures such as holdings and EOR arrangements carry incorporation, maintenance, and compliance costs, and international tax positioning always requires specialised legal and tax advice.

Practical Example: A Director of Photography From Another Country Wants to Live in Portugal

Access to IFICI is not automatic: it depends on registration, qualification under eligible activities, confirmation of the applicable requirements and possible later verification. But once inside the regime, the exemption of certain income qualified as foreign-source appears to operate much more directly than under the former NHR regime.

According to available legal analyses, this exemption does not appear to require proof of effective taxation abroad. The central question is no longer whether the income paid tax abroad, but whether it can be qualified as obtained abroad — and how that qualification is accepted or challenged.

Ben arrives in Lisbon to begin a new chapter — with sun, opportunity, and a very particular tax regime.

Character: Ben, a Director of Photography from another country.

💼 See examples of covered professions and activities

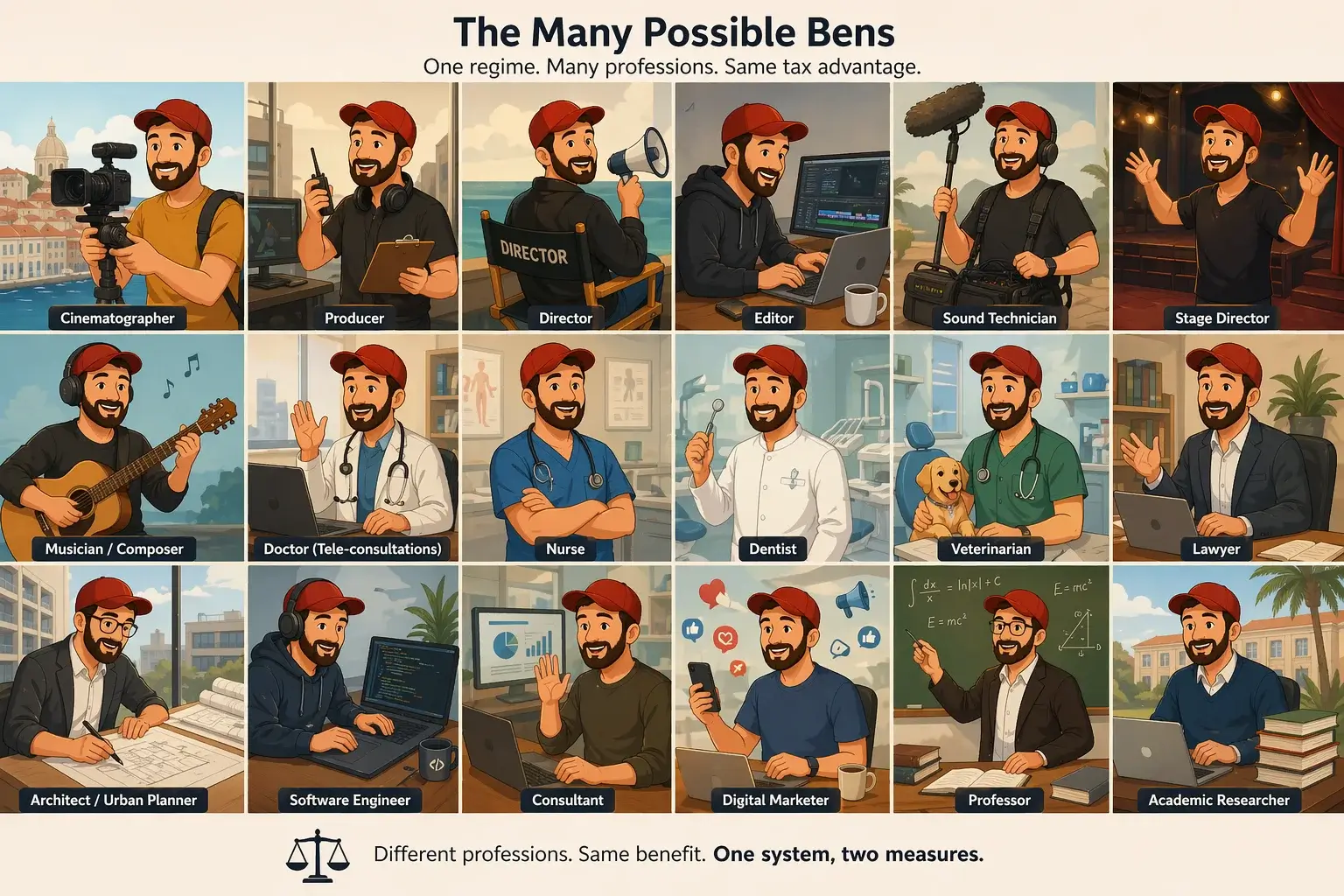

The official lists of qualified positions and relevant economic activities show that the regime may cover a wide range of profiles and sectors, beyond the public narrative centred on science, research and innovation.

General directors and executive managers of companies

Administrative and commercial services directors

Production and specialised services directors

Hospitality, restaurant, retail and other services directors

Specialists in physical sciences, mathematics, engineering and related technical fields

Doctors

University and higher education professors

Finance and accounting specialists

Information and communication technology specialists

Film, theatre, television and radio directors, stage directors, producers and related directors

Intermediate science and engineering technicians and professions

Administrators, managers and general directors of eligible companies

The economic activities recognised as relevant also include areas such as accommodation, restaurants, education, human health, manufacturing, information and communication, consultancy, financial activities and insurance, among others.

Sources: Portuguese Tax Authority information leaflet on IFICI, Notice No. 4812/2025/2 / IAPMEI and Notice No. 5309/2025/2 / AICEP.

Objective: He wants to move to Lisbon and pay the minimum possible tax using the TISRI (NHR 2.0 / IFICI) regime.

Problem: He does not yet have foreign clients.

Solution: Consulting firms offer several legal “paths” to help him fit the regime.

The choice of this profession is not arbitrary: IAPMEI’s Notice No. 4812/2025/2 expressly lists, under code 2654, “film, theatre, television and radio directors, producers and related directors” as eligible for IFICI.

Importantly, the classification of activities — particularly those considered “high value-added” — is not always subject to prior validation and may be assessed later by the Tax Authority, sometimes years after the fact. This creates a layer of legal uncertainty where eligibility can depend on interpretation and be challenged retrospectively.

Path 1 — A Single-Shareholder Company in Portugal

Ben creates a Portuguese single-shareholder company.

He appoints himself manager or director, a role appearing on the list of eligible professions.

The consulting firm ensures that the company invoices more than 50% abroad; in practice, this may only require arranging some international contracts.

Result:

The management salary paid to Ben by the Portuguese single-shareholder company is Portuguese-source income and may benefit from the special 20% rate, regardless of whether the company’s clients are Portuguese or foreign.

Work for foreign clients is often commercially presented as potentially qualifying as foreign-source income and, in certain cases, benefiting from an IRS exemption in Portugal.

Note: Ben can come to Portugal with no clients and, once in Lisbon, begin by securing a few small assignments for foreign clients on his own. That can also count towards the condition that more than 50% of invoicing comes from abroad.

If the work is carried out from Portugal, even for foreign clients, the income will generally tend to be treated as Portuguese-source and therefore not automatically exempt.

What the Portuguese Tax Authority says

The Portuguese Tax Authority itself, in Circular Letter No. 20276/2025, dated 26 February, clarifies that the concept of "job position" referred to in subparagraphs a), b), d), f) and g) of paragraph 1 of Article 58-A of the Tax Benefits Statute " necessarily requires the existence of an employment contract". In practice, this means that a professional invoicing on their own as a service provider, without an employment contract, cannot access IFICI through the routes that depend on a "job position" — which is precisely why the single-shareholder company structure becomes central: it is through that company that the professional can formally become a member of a corporate body of a Portuguese entity, overcoming that formal limitation.

By creating a Portuguese single-shareholder company, Ben stops acting merely as a freelancer and starts offering services across the whole audiovisual field, functioning in practice like a production company capable of competing directly with local companies.

Direct Competition with Local Production Companies

In this position, Ben starts selling services like a genuine film and video production company. When he gets larger projects, he subcontracts local technicians — sound recordists, assistants, operators — and those costs become production costs borne by the company.

On paper, the tax framework makes it possible that:

Foreign clients: the income can be presented as foreign-source income and, in certain arrangements, come close to 0% IRS in Portugal, depending on where the service is effectively provided, on double taxation treaties, and on the Tax Authority’s acceptance.

Portuguese clients: the qualified work Ben provides may, in principle, be taxed at the special 20% rate under the TISRI (NHR 2.0 / IFICI) regime instead of the progressive rates that, for local professionals operating under standard personal taxation, can reach around 48%.

Impact: this tax margin allows Ben to offer substantially lower final prices, even while covering all production costs.

Result: a difference in tax burden is created that, in some scenarios, can amount to dozens of percentage points and which can function as a form of fiscal dumping in a market already weakened by the shortage of employment in Portugal’s audiovisual sector.

Path 2 — A Foreign Holding Company (for example, Malta)

The consulting firm creates a holding company in Malta.

That holding company opens a Portuguese subsidiary.

Ben employs himself in the Portuguese subsidiary and is taxed at 20% on salary.

Profits or dividends from the foreign holding may be paid to Ben with exemption in Portugal, provided treaty rules and economic substance rules are satisfied.

Result:

He satisfies the law formally by having a company, a qualified role, and residence.

But a large share of his income is turned into dividends that are not taxed in Portugal.

Creating and maintaining a holding structure in a country such as Malta may, in general, cost only a few thousand euros per year — registration, virtual office, accounting, company secretarial work, and similar overhead. Those amounts are within reach of many professionals operating under Portugal’s TISRI (NHR 2.0 / IFICI) regime who invoice tens of thousands of euros annually. It is therefore not merely an “exotic scheme for the elite”, but a standardised product that can become economically advantageous from income levels around €30,000 to €40,000, depending on the specific case.

Path 3 — Employer of Record (EOR)

Ben hires a consultant or EOR that creates an entity to “employ” him formally.

That entity invoices services abroad, even if the structure has been assembled specifically for that purpose.

Ben receives salary or fees framed under the TISRI (NHR 2.0 / IFICI) regime and is therefore taxed at 20% IRS.

If he sells his business or has passive income, the consultant may “repackage” those flows into investment products, bringing the effective rate down to 2%–7% in some cases, depending on structure and tax acceptance by the authorities.

Result:

He meets the formal requirements.

But in practice he is using the consultant’s structure in order to gain access to an exemption on foreign-source income.

This issue is not limited to self-employment income. In category A income, a salary paid by a foreign entity may also be presented as foreign-source income. If that income may be taxed in another state under the applicable tax treaty — without having to be effectively taxed there — and Portugal treats it as exempt under the TISRI (NHR 2.0 / IFICI) regime, practical double non-taxation may arise. The Portuguese Tax Authority may, however, challenge this treatment if the activity is effectively carried out from Portugal.

Beyond Employer of Record arrangements, similar outcomes can also be achieved through other structural approaches used in the market.

Crucially, these structural approaches are not merely theoretical. Guidance from leading Iberian law firms indicates that financial activities such as holding companies (under the CAE 6420 classification) may be considered relevant economic activities within the IFICI framework, provided that the applicable conditions are met.

In this context, such structures can be used to establish local economic presence while allowing certain categories of foreign-source income — including dividends — to benefit from exemption, depending on their qualification, applicable tax treaties, and acceptance by the Portuguese Tax Authority.

Path 4 — Already Having Foreign Clients

Example: Ben already works regularly for production companies in his home country and decides to move to Lisbon.

Tax residence: Ben becomes resident in Portugal and applies for TISRI (NHR 2.0 / IFICI) status.

Qualified activity: As a producer, director, or cinematographer, his profession can fit within the TISRI (NHR 2.0 / IFICI) regime as a qualified activity under Ordinance No. 352/2024/1.

Existing foreign clients: He continues to film in Portugal for production companies from his country of origin, invoicing them directly.

Tax declaration:

Although the clients are outside Portugal, Ben performs the work from Portugal. According to the IFICI guide from the Portuguese Order of Certified Accountants, such income is generally Portuguese-source income and is therefore taxed in Portugal under the TISRI (NHR 2.0 / IFICI) regime, not automatically taxed at 0% IRS.

The country of origin taxes only if, under the relevant double taxation treaty, it is allowed to do so — for example, if there is a permanent establishment in that country.

Result:

Work for Portuguese clients is taxed at 20% IRS.

Work for foreign clients may, in some forms of tax planning, come close to an effective burden of 0% IRS.

This type of planning may be presented without the need for a holding company or an EOR, simply by making use of clients Ben already had before moving — although the exemption always depends on the specific tax qualification of the income and may be challenged if the work is performed from Portugal.

In many of these commercial sales narratives, the idea offered to Ben is obvious: settle in Portugal, build foreign relationships and clients, provide them with services from here, and seek to frame that income as foreign-source income that may benefit from an exemption from IRS. These outcomes do not rely on isolated or exceptional configurations, but on combinations of rules that are explicitly embedded in the system.

Path 5 — Minimum Passive Income

Example: Ben has regular foreign passive income — interest, dividends, royalties, rents, or in certain cases gains from the sale of foreign financial assets — adding up to at least €920 per month — the equivalent of the Portuguese minimum wage, used here strictly as an illustrative benchmark.

Tax residence: Ben becomes resident in Portugal and applies for TISRI (NHR 2.0 / IFICI) status.

Qualified activity: A producer, director, or cinematographer may fit within the TISRI (NHR 2.0 / IFICI) regime as a qualified activity under Ordinance No. 352/2024/1. In addition, if Ben receives passive income from foreign sources — such as interest, dividends, royalties, or property rents — such income may, in certain cases, benefit from exemption in Portugal, although each type of income has its own rules and may also be subject to withholding tax in the country of origin. In practice, the tax treatment of certain foreign capital gains may depend on the timing of tax residence, particularly when assets are disposed of after establishing residence in Portugal under the applicable regime. The €920 monthly figure is used here only as an illustrative benchmark for means of subsistence, not as a formal legal requirement.

Continuing to work: Ben continues to work in Portugal as a director or cinematographer. The services he provides, even to foreign clients, are generally taxed in Portugal, though he may benefit from the 20% rate under the TISRI (NHR 2.0 / IFICI) regime if it applies.

Tax declaration:

After entering the regime through his passive income profile, Ben continues to work from Portugal. Even with foreign clients, that labour income is generally considered obtained in Portugal and taxed here, though it may benefit from the 20% rate.

More aggressive tax planning may attempt to build foreign structures in order to reclassify part of that work as foreign-source income and obtain exemption.

Result:

Work for Portuguese clients, and foreign work physically carried out from Portugal, is taxed at 20% IRS.

Foreign passive income may, in some cases, be exempt from IRS in Portugal.

This can happen without any holding company or EOR arrangement, simply through passive income Ben already had outside Portugal.

Comparative Table

Path

What Ben does

How it formally fits the law

What he pays

How it works in practice

Single-shareholder company in Portugal

Creates his own company

Eligible role + activity recognized as relevant (subpara. d), or 50%+ foreign invoicing (subpara. c, ii)

20% in Portugal; abroad may, in some cases, come close to 0%

Declares work for foreign clients as “foreign-source income”

Holding company in Malta

Creates a parent company abroad plus a Portuguese subsidiary

Employment in a qualified role

20% on salary; dividends may, in some cases, be exempt

Profits are distributed as exempt dividends

Employer of Record (EOR)

A consultant creates an entity that employs him

Exporting company + qualified role

20% on salary; investment-packaged income may, in some cases, be taxed at 2%–7%

Passive income is repackaged into investment products

Already having foreign clients

Continues invoicing clients from his home country

Qualified profession + residence

20% in Portugal; abroad may, in some cases, come close to 0%

Frames international invoicing as “foreign-source income”

Minimum passive income

Proves regular foreign passive income of at least €920/month

Residence + qualified profession

20% in Portugal and, in some cases, close to 0% abroad, including eligible foreign passive income

Uses passive income as a base of subsistence combined with the TISRI (NHR 2.0 / IFICI) regime

Conclusion.

Anyone who already has foreign clients only needs to fit within the TISRI (NHR 2.0 / IFICI) framework; the tax benefit can apply immediately.

Anyone who does not have such clients turns to consultants to build structures — single-shareholder companies, holdings, or EOR arrangements — that simulate or generate international invoicing.

Anyone with foreign passive income may, in some cases, benefit from IRS exemption under the TISRI (NHR 2.0 / IFICI) regime, provided they are already framed through a qualified activity and tax residence.

In many cases, the desired effect converges towards a similar outcome: a 20% rate in Portugal combined with reduced or, in some structures, near-zero taxation on certain foreign-source income, depending on legal qualification and treaty interpretation.

IFICI is not fraud, but it is an invitation to inequality — flavoured with pastel de nata and 0% IRS.

The Tax Engineering IFICI Makes Possible

How formal requirements, documentation, corporate structures and international flows can become a fiscal architecture that ordinary residents can hardly replicate.

This section does not claim that these structures are widely used, nor that every arrangement of this kind is illegal.

The central point is something else.

The regime creates interpretative grey areas where consultancies, tax lawyers and international providers may attempt to turn formal requirements into fiscal architecture.

There is an entire professional economy dedicated to exploring, optimising, structuring and defending the possibilities opened by the regime.

An international regime explained almost exclusively by private intermediaries. Although the IFICI is promoted internationally to attract foreign residents, the legislation, the official notices and the mechanisms for practical interpretation remain largely available only in Portuguese. Foreign nationals who have contacted IAPMEI seeking clarification on the regime have received, among others, this reply: "We apologize, but we do not have the legislation in English."

This creates a practical dependence on consultancies, law firms and specialised intermediaries to interpret, structure and access a regime that was designed precisely to attract new international residents — yet whose official documentation remains inaccessible to those who do not speak Portuguese.

ℹ️ European policy context on harmful tax practices

A European Parliament study on harmful tax practices within the European Union does not analyse IFICI specifically, but it provides a useful framework for understanding why regimes of this kind deserve scrutiny. The study identifies several models that may lead to harmful tax competition when structured in a way that distorts the normal allocation of resources within the Single Market — including foreign-source income exemption regimes, shell companies, special economic zones and preferential tax rulings.

These measures are not necessarily illegal in themselves. They become problematic when they produce selective tax advantages, double non-taxation, or outcomes disconnected from real economic activity. IFICI is not analysed in that study, but the combination of foreign-source income exemptions, holdings, EOR arrangements, international structures and benefits reserved for new residents presents characteristics that coincide with risk categories of harmful tax competition identified in the study.

This analysis is not based on identified individual cases, but on the cross-reading of legislation, official notices, technical guidance, consultancy publications, legal analysis and publicly available market patterns. The objective is not to accuse specific beneficiaries, but to show how the architecture of the regime can be interpreted, marketed and structured.

When the difference between the standard regime and IFICI can mean dozens of percentage points in tax, this is no longer an academic issue. There is a clear economic incentive to test the limits of the law: classify roles as strategic, present holding companies as active management structures, distinguish artificially between Portuguese-source and foreign-source income, or organise income flows through intermediary entities.

Even if the Portuguese Tax Authority may challenge some of these arrangements later, the political problem remains: the regime shifts part of the scrutiny to after the fact, while the economic benefit may be captured from the beginning by those with access to specialised advice.

IFICI creates a significant temporal asymmetry: the tax benefit can be obtained from the outset, while full verification of economic substance, the main activity, and the actual eligibility of the structure may occur only later. For some beneficiaries, this transforms the regime into an immediate benefit subject to potential future reinterpretation; for the market, however, the effects on prices, margins, hiring, and competition can materialize long before any tax adjustment takes place.

Holding companies, head offices and active management

One of the least discussed aspects of IFICI is that the regime is not limited to laboratories, universities, scientific research or advanced technology. The official framework also recognises certain financial, insurance, consultancy and business management activities as relevant to the national economy.

Among the listed activities are CAE classes 6420, associated with holding companies, and 7010, associated with head office activities — including the supervision and management of other units of the group in the areas of strategic and organisational planning. At the same time, qualified positions include administrators, managers, managing directors and executive managers.

In practice, this means that a new resident may not need to be a researcher, scientist or engineer to access the regime. It may be enough to perform a qualified role or sit on the governing body of a qualifying entity, provided the formal requirements are met and accepted by the competent authorities.

This is where the line between an innovation incentive and aggressive tax planning becomes politically relevant. A merely passive holding company would be difficult to justify under the regime — but a structure that provides management, coordination or direction services to its subsidiaries may present itself as a qualifying economic activity, creating a bridge between tax residence in Portugal, administrative functions and income structured through corporate entities.

The distinction matters precisely because eligibility depends on formal framing, functional description, main activity, contracts, documentation and later interpretation. The question is no longer only “what does this company actually do?” but also “how is that activity described, documented and presented to the competent authorities?”. That difference may be legitimate in some cases; in others, it can become a way of moving an aggressive tax planning structure closer to a benefit publicly presented as supporting innovation and value creation.

The political problem lies in that boundary. If access to the benefit depends heavily on how the activity is organised and described, then those able to pay for specialised consultants gain an additional advantage: not only a tax advantage, but an interpretative one.

The many faces of the tax advantage

The example of Ben as a director of photography is only a narrative entry point. The broader problem is that the regime may accommodate very different profiles, provided they can be framed within one of the formal or interpretable categories available under it.

1. Creative Ben

A film director, producer, cinematographer or audiovisual professional with international clients, presented as a qualified activity or an exporter of services.

2. Academic Ben

A PhD holder, researcher, lecturer or technical specialist whose academic profile can reinforce the narrative of research, innovation or high added value.

3. Founder Ben

A founder, administrator or member of the governing body of a certified startup, using the innovation narrative to access the regime.

4. Manager Ben

An administrator, manager or director of a qualifying company, including management structures, head offices or holding companies presented as active entities.

This diversity matters politically. The more profiles can fit into the regime, the weaker the public narrative becomes that IFICI is merely a narrow incentive for scientific research and innovation. And the more qualified, internationalised and advised the beneficiary is, the greater the ability to combine those doors into a highly optimised fiscal arrangement.

When tax optimisation becomes a product

The pattern that emerges from these interpretations is consistent: IFICI does not merely reduce tax rates — it creates a grammar of classification. The same economic reality can be reorganised through different labels (startup, head office, shared services centre, exporting company, active management holding, qualified researcher, administrator, specialised technician) and recombined into fiscal narratives ready to be sold as a structurable product, not merely as a public policy for innovation.

It is this elasticity that makes IFICI particularly attractive to consultants and tax lawyers. The product being sold is not merely a 20% rate or a possible exemption on foreign-source income. It is the ability to redesign the taxpayer’s fiscal story so that it fits one of the available doors.

It is in how easily market language turns the regime into pathways, vehicles, structures, economic substance, management contracts and competitive advantages. Public policy promises innovation; the commercial ecosystem quickly learns to sell it as tax positioning.

The problem is not that all these pathways are necessarily illegal. The problem is that the distance between real economic activity and an optimised fiscal narrative can become small enough to be turned into a professional service. This is where IFICI stops being merely a tax benefit to attract talent and starts functioning as a platform for fiscal design: those with access to the right consultants do not merely declare their activity — they learn how to frame it.

A documented case study

A particularly revealing example can be found in a public account published by a Portuguese law firm concerning the creation of a venture builder. According to the firm’s own description, after the end of the former NHR regime it examined the new IFICI qualification routes and identified membership of the governing body of an active certified startup as a possible pathway for expatriate clients.

According to the published explanation, participating clients contribute capital, professional experience and contacts, join the company’s governing body and use that position as the basis for applying to IFICI. The firm later publicly stated that approximately 50 of its IFICI clients had been approved.

The unusual feature is the integration of the entire pathway.

The legal adviser, the qualifying entity, the investment opportunity, the governing-body position and the IFICI application appear to form part of the same commercially organised ecosystem.

This does not, by itself, demonstrate illegality, the absence of genuine business activity or that the participants perform merely nominal functions. It does, however, show how access to eligibility can itself become part of a structured professional service: a client seeking the tax regime is introduced to an entity created within the adviser’s ecosystem, invests in it, assumes a potentially qualifying position and is then assisted by the same adviser in obtaining registration.

The publicly available information does not make it possible to determine how much each participant invests, which amounts correspond to investment or professional fees, how members of the governing body are selected, what individual responsibilities they assume, how much time they devote to the company or whether those positions would exist independently of IFICI.

The public presentation of this venture builder also provides limited evidence from which to assess the scale and maturity of its activities. Its website consists essentially of a single institutional page listing seven portfolio projects. Only two link to external websites, and both are classified as investments rather than ventures developed internally by the studio. The remaining projects have no dedicated pages, identified teams, public product demonstrations or independently verifiable operating indicators.

This limited public information does not prove that the projects lack genuine activity. It does, however, prevent an independent assessment of their maturity, economic substance, measurable results and the individual contribution made by the governing-body members whose positions support IFICI applications.

This example concerns one particular pathway — investment combined with participation in the governing body of a certified startup. More broadly, when the different pieces of IFICI structuring are assembled, the architecture can take a recognisable shape: a formal entity in Portugal, an eligible activity, documented economic substance, organised international invoicing, separated salary and dividends, and foreign income framed within an exempt category.

1. The vehicle

A Portuguese company, head office, holding company, startup or production entity is used as the formal structure through which the activity is framed.

2. The narrative

The activity is described as innovation, active management, research, export of services, curation, qualified production or a high added-value function.

3. The substance

Contracts, coworking arrangements, minutes, reports, emails and functional descriptions, among others, are used to try to demonstrate that the structure has presence and real activity.

4. The extraction

Economic income can be divided between salary, dividends, capital income, foreign entities and international flows, seeking to reduce income tax and contributions.

This is one of the hardest aspects to explain to the public, but also one of the most important: the problem is not only the money that comes in, but the fiscal label under which it enters. The same economic reality can be presented as work, management, investment, dividend, intellectual property or foreign income, depending on the structure built around the beneficiary.

Interactive editorial simulator about the decision path commercially presented around IFICI. Currently available in Portuguese. Click the image to open the tool.

The problem is not one isolated piece.

It is the whole: when vehicle, narrative, documentary substance and international flows combine, the regime may stop functioning merely as an innovation incentive and start operating as an architecture of fiscal invisibility.

This reading does not require claiming that all beneficiaries abuse the regime. It is enough to recognise that the law creates a sequence of formal doors that can be organised by specialised consultants to produce a fiscal and contributory burden that most ordinary residents can never replicate.

Economic substance or documentary theatre?

One of the most sensitive areas of this kind of planning is so-called economic substance. In theory, a legitimate structure must demonstrate real activity, decision-making capacity, adequate resources, effective management and an economic link to the territory. In practice, however, the boundary may depend on documents: contracts, minutes, reports, emails, proof of physical premises, functional descriptions and files prepared to withstand a possible tax inspection.

This is where the critique of the regime becomes more concrete. A merely passive holding company may be difficult to justify. But a holding company presented as an active management centre, with a coworking contract, decision minutes, consultancy services, intra-group invoicing and periodic reports, may attempt to build the appearance of sufficient operational activity to defend the arrangement.

The same applies to the export requirement. When a Portuguese company invoices management, consultancy or production services to foreign entities related to the beneficiary himself, the issue is no longer only tax-related: it also involves transfer pricing, economic justification for the amounts charged and proof that the services were actually provided under conditions comparable to the market.

This is the critical point: the greater the tax advantage, the greater the incentive to produce the documentation that makes the structure defensible. Economic substance then stops being merely a business reality and also becomes a documentary construction.

The question is no longer only “is there real activity?”.

It also becomes: what activity was described, what contracts were drafted, what minutes were produced, what prices were justified and what narrative was prepared to convince the competent authorities?

The greater risk is performative compliance.

When the focus shifts to preserving traces of presence, producing minutes, preparing reports, justifying prices, organising emails and building documentation to withstand a future inspection, the boundary between real activity and documentary staging becomes politically impossible to ignore.

The problem becomes even more serious when the strategy is no longer only to meet requirements, but to manage risk signals: avoiding inconsistencies between declared income and lifestyle, deciding when to request or avoid refunds, preparing annual activity reports, organising evidence of physical presence and building a documentary narrative before any audit takes place.

In creative, scientific or intellectual sectors, this boundary becomes even harder to audit, because the value of the work can be described as research, curation, strategy, artistic direction, qualified production or highly specialised technical merit.

At that point, substance is no longer only what the company actually does. It also becomes what it can prove, archive, report and stage through documentation.

None of this means that all these structures are false or abusive. But it shows how a regime with significant benefits, broad categories and documentary validation can create an industry of framing: not only to comply with the law, but to build the version of reality that best fits it.

From fiscal dumping to contributory dumping

The public discussion around IFICI tends to focus on personal income tax: 20% on certain qualifying income and possible exemption on certain categories of foreign-source income. But tax engineering around the regime can operate on two additional layers: social security contributions and the international routing of income.

1. Low salary, high dividends: contributory dumping

The logic: maintain a formal remuneration subject to income tax and social security contributions, while a substantial part of the economic income is extracted through dividends, profits or capital income.

The effect: the advantage is no longer only a lower income tax rate. It may also reduce the effective participation in the financing of Social Security.

The risk: if the formal remuneration is artificially low compared with the real functions performed, the structure may be challenged by the authorities.

The logic: income that would not directly benefit from exemption because it comes from sensitive jurisdictions may try to circulate through intermediary entities in non-listed countries.

The effect: the income arrives with a fiscal appearance that differs from its real economic origin.

The risk: CFC rules, anti-abuse clauses, beneficial ownership, economic substance and transfer pricing may lead the Portuguese Tax Authority to disregard the structure.

The advantage is not only in paying less personal income tax.

It is in the ability to separate salary, dividends, capital income, social contributions, jurisdiction of origin and paying entity — an architecture that the ordinary local worker can rarely replicate.

This is why the critique of IFICI cannot be limited to the 20% rate. The regime becomes politically explosive when it allows a reduced rate on qualified work to be combined with exemptions on foreign income, corporate structures, dividends, intermediary entities and reduced social contributions.

And there is a layer above this one. IFICI does not exist in isolation: a sophisticated beneficiary may stack the personal income tax regime with corporate tax incentives such as SIFIDE (R&D deductions), sectoral support schemes such as the audiovisual cash rebate, and differentiated treatments for salary, dividends, profit-sharing, royalties and copyright income — each legitimate on its own, but cumulatively powerful.

The problem is not the isolated existence of each incentive.

The problem is the cumulative effect: when personal, corporate, sectoral and contributory benefits can be combined, the advantage stops being merely fiscal and becomes systemic.

This accumulation does not, in itself, imply illegality. Many of these instruments have legitimate goals: attracting investment, supporting audiovisual production, encouraging research or rewarding productivity. The political question is who has the capacity to combine them, for what purpose, and what kind of competition this creates against local professionals and companies operating without the same fiscal and advisory architecture. When the effective tax, contributory and financial burden can be reduced through multiple channels at the same time, competition no longer depends only on talent, price or quality: it also depends on the ability to structure, finance and absorb margins differently from local competitors.

The checklist reveals the problem.

What looks complex when described legally becomes simple when organised as a process: create the vehicle, choose the framing, produce substance, structure remuneration, justify prices, monitor ratios and prepare documentation. The political issue is precisely that: when fiscal inequality can be turned into a consultancy checklist, it stops looking like an exception and starts functioning as a product.

There is an essential distinction underlying everything above: IFICI is not an accidental flaw in the system. The 20% rate, the exemption of certain foreign-source income and the openness to management activities, head offices, holding companies, startups, research and qualified roles are part of the political design of the regime.

The declared objective is to make Portugal competitive in the international race for talent, investment and highly mobile residents. In that sense, the legislator accepts a trade-off: giving up part of normal taxation in exchange for the promise of attracting people, capital, consumption, companies and economic activity.

The problem begins when this logic of fiscal competitiveness becomes broad enough to accommodate structures whose main value lies not in innovation created in Portugal, but in the ability to organise income, functions, companies and documents in a tax-efficient way.

The political question is not only whether there is abuse.

It is why the law creates a regime where the boundary between legitimate incentive, aggressive planning and structural inequality so often depends on interpretation, documentation and the ability to pay for specialised advice.

In this sense, the critique of IFICI is not only moral or fiscal. It is a critique of the model of competition between states: countries compete for mobile residents by offering preferential regimes, while ordinary residents remain inside the general system that funds public services, Social Security and collective life.

The critical point is not that a holding company is automatically eligible.

The critical point is that the regime contains formal pathways through which holding, management and administrative structures can be brought closer to a tax benefit publicly sold as science, research and innovation.

The inversion is this: the law's stated objective is to attract talent, research and innovation. In practice, however, the regime also creates a market for those with enough capital to pay lawyers and consultants capable of designing structures suited to the tax benefit. Situations arise in which what is sold is not talent but structure. And it is the structure that captures a meaningful share of the fiscal rent released by the regime.

The LX Launch model provides a concrete public illustration of this concern: the taxpayer does not necessarily arrive with a pre-existing qualifying position. The adviser’s ecosystem may itself provide the entity, the investment route, the governing-body role and the professional assistance required to submit the IFICI application.

The result is a self-sustaining ecosystem: the regime breeds complexity; complexity breeds technical dependence; technical dependence breeds premium services; premium services breed structuring; structuring breeds risk; and risk breeds more advisory work, amended tax returns and litigation.

For a concrete illustration of how the regime is presented by the legal sector itself as a corporate restructuring exercise rather than a mere individual tax incentive, see “The C-Suite Migration to Portugal: Why IFICI is a Strategy, Not Just a Tax Break”, published by LVP Advogados.

Living in Portugal while earning passive income from abroad — potentially with little or no Portuguese personal income tax.

Living in Portugal on Foreign Passive Income

Ben receives passive income, such as rent from a property in his home country, amounting to at least one Portuguese minimum wage (€920 in 2026). He lives in Portugal and is covered by the NHR 2.0 / IFICI regime.

Ben does not work and still has access to the social safety net and to public services financed by the taxes — IRS, VAT, and others — paid by standard tax residents, while his own contribution to IRS may be 0%.

The central issue is not consumption or property taxes, but the absence of income tax — the core of the Portuguese tax system and its progressive structure.

In its real‑world application, the regime mainly attracts qualified residents or individuals with financial means, and it does not include any mechanism for annual verification of activity.

In theory, IFICI requires the beneficiary to continue performing a qualifying activity in order to maintain the regime. In practice, there does not appear to be any automatic annual verification of that activity through the tax return process, meaning that foreign passive income may continue to be declared as exempt while the status remains active, unless reviewed by the Portuguese Tax Authority.

Reminder: consult a tax specialist; this text does not replace professional advice.

Housing Pressure and the Ben–Zé Divide

The Ben–Zé contrast does not end with income tax. It extends directly into the cost of living — particularly housing, where Portugal has experienced one of the most aggressive price increases in Europe over the last decade.

Ben arrives under a preferential tax framework. In some cases, he may retain a significantly higher share of his income than a standard tax resident doing the same work. Zé, by contrast, remains subject to the ordinary tax system while facing the same rents, the same property market, and the same daily costs. The result is not just fiscal asymmetry, but unequal purchasing power inside the same city.

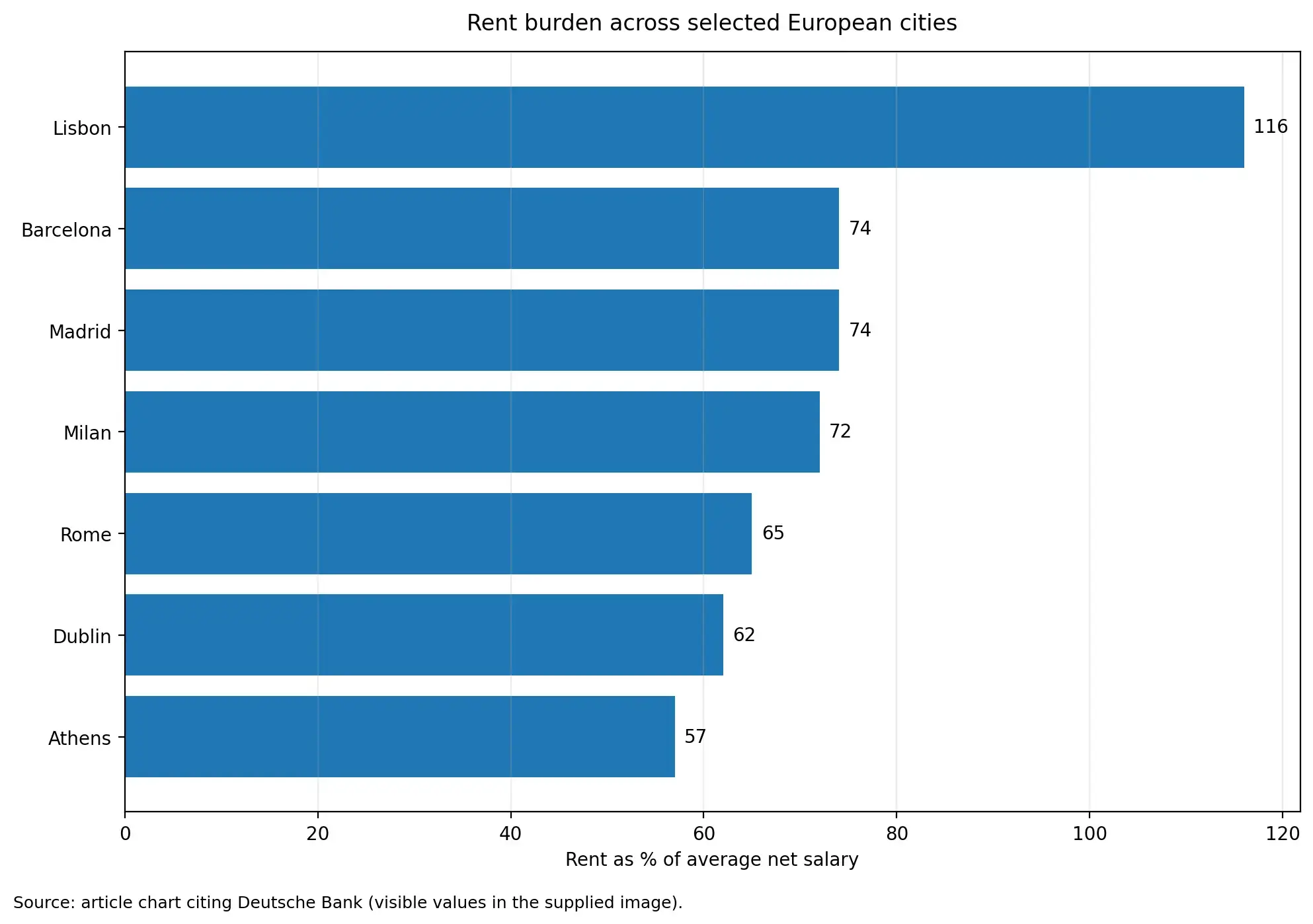

Lisbon stands out as one of the most extreme cases in Europe, with rent levels reaching or exceeding 100% of average income. Source: Deutsche Bank (via published analysis).

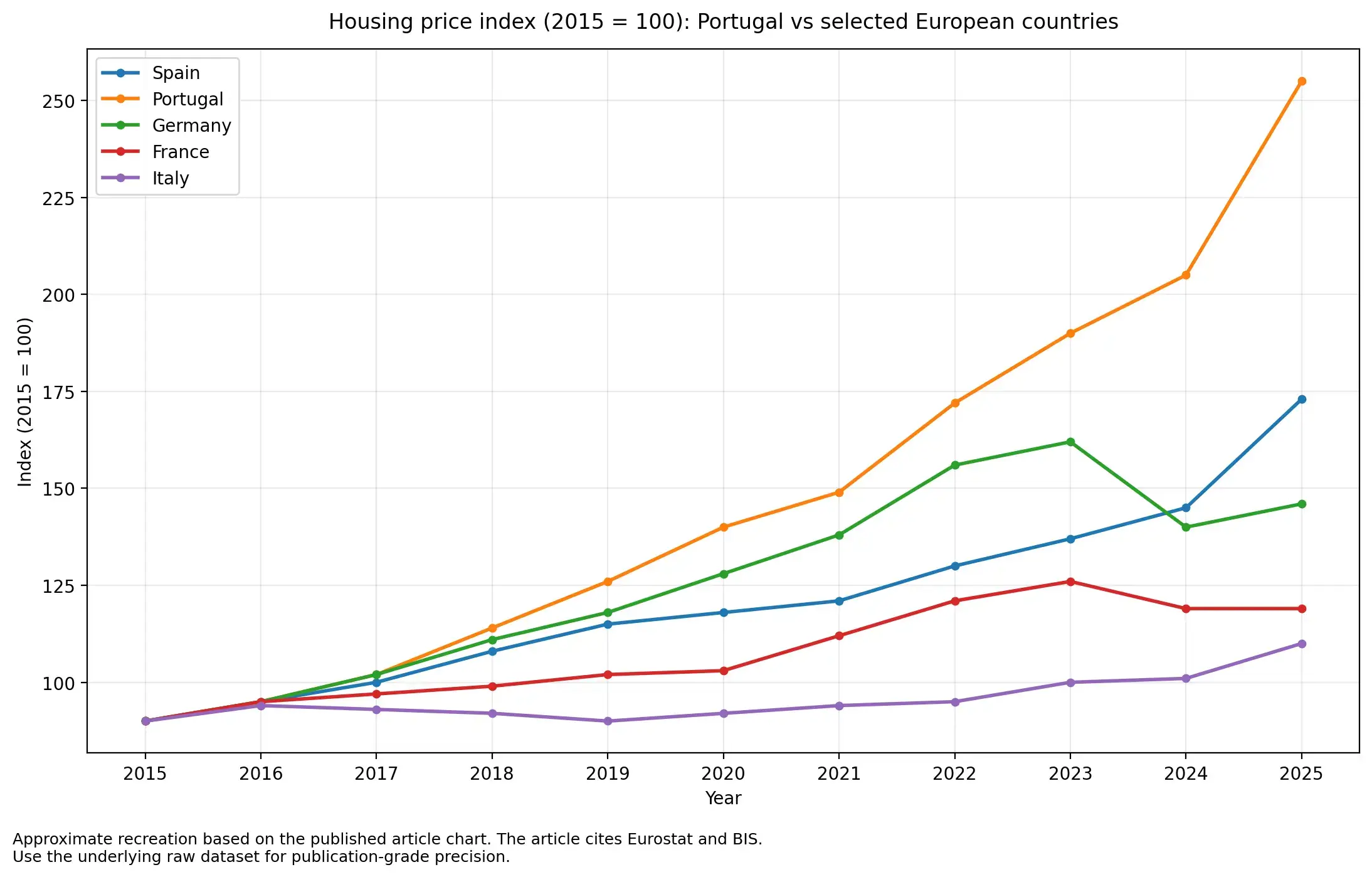

At the same time, housing prices in Portugal have risen faster than in comparable European economies. While the European Union has seen significant increases, Portugal shows a clear divergence, with price growth outpacing countries such as Spain over the same period.

Portugal has experienced one of the steepest housing price increases in Europe since 2015. Approximate editorial recreation based on published data (Eurostat / BIS framework).

In this context, even a relatively modest tax advantage can have outsized effects. If Ben retains more net income than Zé, he can absorb higher rents, compete more aggressively for housing, and remain in central urban areas. Zé, meanwhile, is squeezed from both sides: higher taxation on one side, rising housing costs on the other.

This is not driven by a single cause. Housing inflation is driven by multiple factors, including supply constraints, tourism, global capital flows, and investment dynamics. However, when a tax regime selectively increases the purchasing power of some residents in already constrained urban markets, it may amplify existing pressures.

In that sense, the Ben–Zé divide is not only fiscal. It becomes spatial: a question of who can still afford to remain in Lisbon, and who is gradually priced out while competing under less favourable conditions.

For years, several real estate stakeholders argued that regimes such as NHR had no meaningful impact on housing prices in Portugal. However, when the end of the regime was announced, some of those same actors began warning about a potential drop in foreign demand and a possible stabilisation of prices.

This shift in narrative implicitly suggests that the regime may, in fact, have contributed to pressure on the housing market — not as a single cause, but as an additional factor within a context already shaped by supply constraints, tourism, and international capital flows.

This tension between public messaging and market reaction reflects a broader challenge in assessing the real impact of such regimes: while their effects may be difficult to isolate, their influence becomes more visible when they are removed.

A Contradiction That Is Hard to Ignore

From a tax law perspective, this raises questions related to the principle of ability to pay and fiscal equality. When individuals operating in the same market are subject to substantially different effective tax rates based on formal eligibility criteria, the outcome may conflict with the idea that taxation should reflect comparable economic capacity. The existence of international tax competition helps explain why such regimes are implemented, but does not in itself resolve the question of their fairness within the domestic system.

In theoretical terms, such regimes may generate broad gains when adopted unilaterally. However, in a context where multiple countries apply similar policies simultaneously, the overall effect may be to reduce redistributive capacity and concentrate gains among highly mobile, high-income individuals.

Part of this contradiction also stems from the interpretive nature of the regime itself. While the legal framework defines formal eligibility criteria, its application — particularly regarding the qualification of income and cross-border situations — has been subject to differing interpretations between the Tax Authority and the courts, creating uncertainty and room for divergent outcomes in practice.

If the work is physically done in Portugal, why is the tax logic not the same for everyone?

If the relevant criterion were the place where the work is actually performed, the Portuguese Tax Authority would have to apply the same logic to everyone: to the Portuguese director who has always lived in Lisbon and to Ben, the “new digital nomad”, sitting at a café table editing videos for a client in New York. In both cases, the work is carried out in Portugal.

And yet the TISRI (NHR 2.0 / IFICI) regime opens an exception precisely for certain Bens, allowing a large part of that income to be treated as “foreign-source” and therefore potentially exempt from IRS, while standard tax residents remain under normal taxation. Either the income is Portuguese for everyone, or it is foreign for everyone. Anything else amounts to discrimination built into the law itself.

The use of foreign intermediary companies only makes the whole arrangement more artificial. In practice, it can work like this: the client is Portuguese, the work is done in Portugal, but the invoice comes from a foreign company for which Ben “works” — whether that company is a producer or a holding in a place such as Malta. That foreign company invoices Ben’s client and then pays Ben. In the end, the entire income appears to come from abroad even though the work never left Lisbon.

As for content-based distinctions, there is no clear and objective legal criterion capable of saying: “up to this point it is documentary; beyond that it becomes advertising or corporate video.” In substance, it is all audiovisual production within the same professional family.

International Work and the “Loophole”

For many freelancers and local production companies providing the same services as Ben, international work is one of the main sources of income and growth. When the TISRI (NHR 2.0 / IFICI) regime gives a far greater tax advantage only to newly arrived qualified residents, it creates unequal competition exactly in the space where domestic talent has been trying to grow.

Moreover, competition for the same clients does not stop at the international market: Ben can use this tax advantage to offer lower prices to Portuguese clients too, gaining an advantage in both markets.

In this example, by not being taxed in the client’s country — being treated there as a non-resident under the relevant treaty, perhaps by means of forms such as the W-8BEN — and by being exempt in Portugal under the TISRI (NHR 2.0 / IFICI) regime, Ben can reach situations approaching double non-taxation.

A concrete precedent